Key Points

- The “Pay Yourself First” Rule: Stop trying to save what’s “left over” at the end of the month. Use Reverse Budgeting by automating your 401(k) or IRA contributions to leave your paycheck before you even see it. This removes the “willpower” struggle and forces your lifestyle to adapt to the remaining balance.

- Time is Your Greatest Asset: In retirement math, when you start is more important than how much you start with. Because of compound interest, a dollar invested in your 20s has roughly 10x the growth potential of a dollar invested in your 40s. Starting small today is mathematically superior to starting large a decade from now.

- Diversify to Defend: Don’t gamble your future on a single stock or a low-interest savings account. Use a mix of Total Market Index Funds and Roth IRAs to protect yourself against market volatility and future tax increases. High diversification acts as a financial shield for your long-term wealth.

In 2026, the traditional view of retirement is being completely rewritten. The dream of a gold watch and a guaranteed pension has been replaced by the reality of longer lifespans, evolving work models, and a do-it-yourself savings landscape. As of early 2026, the US Bureau of Labor Statistics reports that private industry employer costs for retirement and savings plans have shifted significantly, placing more weight on individual contributions than ever before. Furthermore, with the Social Security Administration’s 2026 Cost-of-Living Adjustments (COLA) struggling to keep pace with specific service-sector inflation, the “do-it-yourself” mandate has never been more urgent.

Recent data from the Federal Reserve’s Economic Well-Being of U.S. Households suggests that while more Americans are participating in 401(k) plans, nearly 28% of non-retired adults still feel their retirement savings are not on track. This shift has made it crucial for every American to become an active architect of their own financial future.

But here’s the most important takeaway: building your retirement nest egg is not a sprint; it’s a marathon where consistency is your greatest superpower.

This is The Ultimate Guide to Retirement Savings—a human-centric blueprint designed for real people navigating a rapidly changing economic landscape. Whether you are twenty-four, forty-four, or fifty-four, this guide will provide a personalized strategy for every decade of your career, showing you exactly how small, deliberate actions today can create massive financial freedom tomorrow. We will move beyond the complex jargon to find the simple, sustainable steps that work for you.

To show you exactly why this guide is essential, let’s look at the defining financial realities of retirement planning in the United States today.

Related: Emergency Funds in the Age of Buy Now, Pay Later (BNPL)

Related: Emergency Funds in the Age of Buy Now, Pay Later (BNPL)

The New Math of American Retirement in 2026

The traditional advice to “save 10%” is no longer sufficient. Today’s reality is shaped by three unstoppable forces: Inflation, Longevity, and Market Volatility.

To understand why a proactive strategy is your only option, consider these critical statistics:

-

Inflation’s Hidden Tax: In 2026, a $1 million retirement goal has the purchasing power of only **$680,000** in 2020 dollars (assuming a steady 3.5% inflation rate). What seemed like a fortune ten years ago is now the baseline for a comfortable, not luxurious, retirement.

-

The “DIY” Mandate: The portion of the US workforce covered by a traditional defined-benefit pension has plummeted to less than 15% in 2026, according to the Bureau of Labor Statistics Pension Coverage Data. The responsibility for your retirement income now rests squarely on your shoulders.

-

The Longevity Reality: A 65-year-old couple retiring in 2026 has a 50% chance that at least one spouse will live to age 92, according to the Society of Actuaries Longevity Studies. This means your savings must last for a 30-year “non-working” period.

-

Market Volatility is the New Normal: Relying on linear 7% growth projections is a dangerous gamble. The post-2024 economic cycle has been defined by high-inflation “pockets” and significant sector rotations, making active diversification non-negotiable.

This data paints a clear picture: “Saving” is no longer enough. You must become an automated, disciplined, and strategic Investor.

Phase 1: The Foundation — Mastering the Savings Mindset

Before we discuss which accounts to open or which funds to buy, we must address the single biggest bottleneck to retirement success: Human Psychology.

The human brain is wired for immediate reward, not deferred satisfaction. This is known as Present Bias, and it is the reason that 78% of Americans report having “financial anxiety” while simultaneously struggling to build an emergency fund.

The solution is not more willpower; it is automation.

Hack Your Behavioral Psychology

If you have to choose every single month between funding your 401(k) and enjoying your income today, your 401(k) will lose eventually. The strategy of Reverse Budgeting (or “Paying Yourself First”) bypasses this entirely. By setting up an automated transfer that moves 15% (or whatever your goal is) from your paycheck before it even hits your checking account, you remove the decision entirely. You adapt your lifestyle to the 85% remaining, turning saving from a monthly battle into a background process.

Phase 2: Building Your Account Toolkit — Knowing Your Options

Your choice of “vehicle” (the account type) is just as important as the money you put into it. The primary difference between these accounts is Tax Treatment.

The Employer-Sponsored Plan (401k or 403b)

This is the bedrock of most retirement plans. Your contributions are made pre-tax, which reduces your taxable income today. The money grows tax-deferred until you withdraw it in retirement, at which point it is taxed as regular income.

-

The Golden Rule: You must contribute at least enough to capture your Employer Match. If your company matches the first 5% of your salary, and you only contribute 4%, you are literally throwing away free money. In 2026, over 20% of employees still miss their full match, according to the Vanguard ‘How America Saves’ Report, costing them thousands in compound interest.

The Individual Retirement Account (The Traditional IRA)

An IRA is an account you open yourself. Like a 401(k), a Traditional IRA allows for pre-tax contributions (if you meet income eligibility) and grows tax-deferred. It is an excellent option if your employer does not offer a 401(k), or if your 401(k) has high fees or poor investment choices.

The Roth Options (Roth 401k or Roth IRA)

This is the strategic favorite of younger investors. Contributions to a Roth account are made post-tax. You get no tax break today. However, the money grows tax-deferred, and your qualified withdrawals in retirement are 100% Tax-Free. The value of the Roth option is massive in 2026, as we are navigating an era of historically high government debt, making it highly probable that income tax rates will be higher when you retire than they are today. A Roth IRA is your hedge against future tax increases.

Phase 3: What to Buy — The Core of Your Investment Strategy

Opening an account is not enough. Your contributions must be invested. If your money is just sitting in a 401(k) settlement fund (basically a 0.01% cash account), inflation is slowly eating it alive.

The Magic of Compounding and Time

Consider this: $5,000 invested at age 25 with a 7% average annual return becomes over $75,000 by age 65, without you ever adding another dollar. Time is your greatest asset. Waiting just 10 years to start means you would need to invest $2.5x more per month to end up with the same amount.

The Passive Revolution: Index Funds and ETFs

You do not need to be a Wall Street genius to succeed. In 2026, the data is overwhelming: Passive Investing (buying the whole market) outperforms Active Investing (picking stocks) over the long term.

For 90% of investors, your “portfolio” can be as simple as two or three funds:

-

A Total US Stock Market Index Fund: You instantly own a small piece of nearly every public company in America.

-

A Total International Stock Market Index Fund: This gives you critical diversification, offering protection if the US market underperforms.

-

A Total US Bond Market Fund: As you get closer to retirement, you add this to reduce volatility.

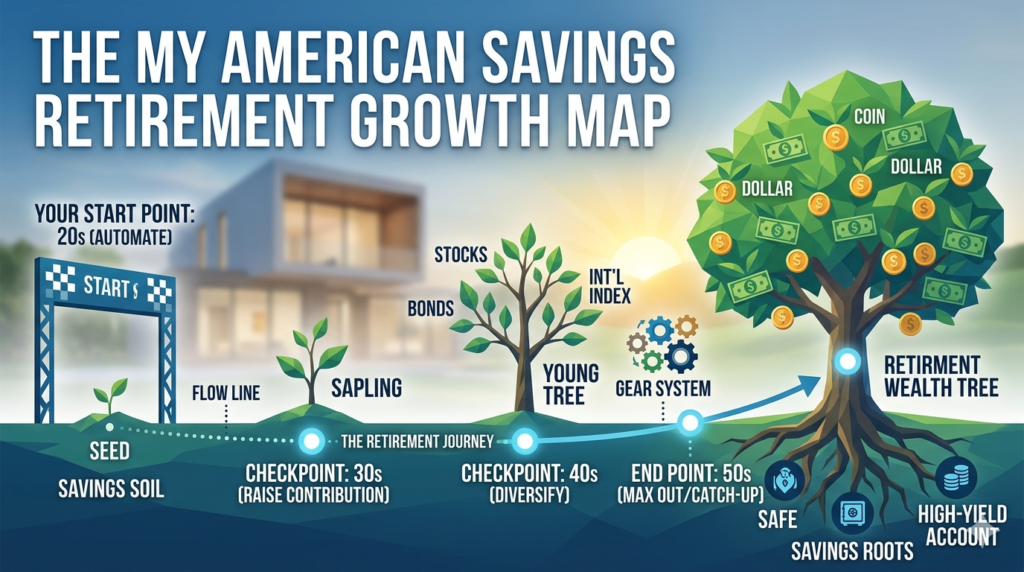

Phase 4: Your Strategy by Decade — A Blueprint for Every Career Stage

Your 20s: Automate, Automate, Automate

-

The Mission: Turn saving into an identity. Your salary may be low, but your “time asset” is at its maximum.

-

The Actions: Set your 401(k) contribution to at least get the employer match. Open a Roth IRA and set an automated contribution of $100/month. You won’t miss the $25/week, but the 40-year compounding runway is priceless.

Your 30s: Increase Contribution and Diversify

-

The Mission: Combat “Lifestyle Creep” and maximize growth. Your salary is likely rising.

-

The Actions: Aim to increase your total retirement savings (401k + Roth) to 15% of your gross income. Audit your lifestyle for hidden expenses and subscriptions. Take our Money Personality Quiz to identify if you are a “Balanced Planner” or a “Developing Saver.”

Your 40s: Strategic Debt Management and Market Hedge

-

The Mission: Balance competing priorities (kids’ college, mortgage) while maintaining your savings trajectory.

-

The Actions: This is where retirement planning gets “real.” Ensure you have a substantial emergency fund. If you have high-interest credit card debt, you must clear it. This is also the time to refine your allocation, adding a modest international bond exposure for defensive diversification.

Your 50s: The Max-Out and Catch-Up Phase

-

The Mission: Maximum contribution and preparing for the “Distribution Phase.”

-

The Actions: In 2026, the Catch-Up Contribution for those over age 50 is $7,500 (allowing a total 401k contribution of $30,500/year). Your mission is to max this out. Use your editorially fact-checked savings calculator to run realistic simulations of your future withdrawal rate (e.g., the “4% Rule”).

Phase 5: Common Retirement Pitfalls to Avoid

As you build your nest egg, several “stealth” traps can derail your progress. Avoiding these common mistakes is just as important as choosing the right investments.

The “Early Withdrawal” Trap

When changing jobs, many people are tempted to “cash out” their 401(k). This is one of the most destructive financial moves you can make. Not only do you pay immediate income tax on the balance, but you also pay a 10% early withdrawal penalty. Most importantly, you kill the “compounding engine” that would have turned that $10,000 into $100,000 over the next twenty years. Always opt for a Direct Rollover to your new employer’s plan or an Individual Retirement Account (IRA).

Ignoring the Impact of Fees

A 1% difference in annual fees might sound small, but over 30 years, it can eat up to 25% of your final portfolio value. Always check the Expense Ratio of the funds you own. In 2026, there is no reason to pay more than 0.10% for a broad stock market index fund. If your 401(k) only offers expensive “actively managed” funds, talk to your HR department or consider focusing your additional savings in a low-cost IRA.

Overestimating Social Security

Social Security was never designed to be your sole source of income. It was intended to be a safety net, replacing roughly 40% of the average worker’s pre-retirement earnings. In 2026, the Social Security Trust Fund faces long-term solvency challenges, which may lead to reduced benefits or higher retirement ages in the future. Treat Social Security as a “bonus” rather than the core of your plan.

Phase 6: Integrating Social Security into Your Vision

While Social Security isn’t a complete solution, it is a vital component of the American retirement puzzle. The timing of when you claim your benefits can change your financial outlook by hundreds of thousands of dollars.

The Power of Waiting

You can claim Social Security as early as age 62, but doing so results in a permanent reduction of about 30% compared to your “Full Retirement Age” (which is 67 for those born after 1960). Conversely, for every year you wait beyond age 67 (up to age 70), your benefit increases by 8% per year.

If you have longevity in your family or have other savings to live on in your late 60s, waiting until 70 is often the single best “investment” you can make. It provides a government-backed, inflation-adjusted annuity that lasts as long as you do.

Phase 7: The Mental Shift — Saving is Freedom

The biggest mistake you can make is viewing retirement savings as a monthly penalty. It isn’t. Your 401(k) and Roth IRA are your personal Wealth Creation Engine. Every dollar you automate today is not “gone”; it is simply being sent ahead to build the life you want tomorrow.

A well-funded retirement isn’t about being rich; it’s about being independent. It means that when you reach your 60s, your lifestyle is determined by your choice, not your necessity.

Your mission today is simple: Start. If you can only save 1%, save 1%. Then, next year, save 2%. The habits you build today are far more valuable than the initial dollar amount. Automation will build the structure; consistency will provide the results. Your future self is waiting for you to begin.

Sources:

-

Inflation purchasing power data: Based on the US Bureau of Labor Statistics (BLS) Consumer Price Index (CPI) Inflation Calculator, adjusted for 2026 purchasing power projections.

-

Retirement Longevity Data: Society of Actuaries (SOA) Longevity Risk Report and US Social Security Administration Life Expectancy Calculators.

-

Pension Coverage Statistics: US Bureau of Labor Statistics (BLS) National Compensation Survey: Employee Benefits in the United States Pension Plan Coverage Data.

-

Employer Match and Contribution Rates: Vanguard ‘How America Saves’ 2025 Report.

-

Social Security Solvency and Benefits: Social Security Administration (SSA) Trustees Report Summary.

Disclaimer:

The information provided on MyAmericanSavings.us is for educational purposes only and should not be construed as financial, investment, or legal advice. Please consult with a licensed professional before making any financial decisions.