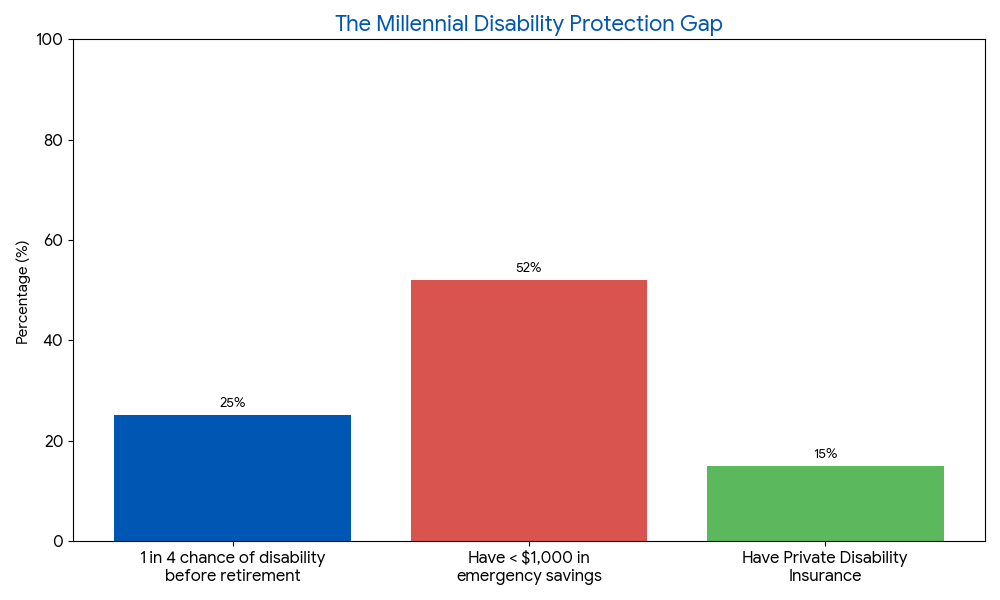

When you’re in your 20s or 30s, the word “disability” usually feels like something that happens to other people—or at least something that won’t happen until you’re much older. We focus on our side hustles, our 401(k) contributions, and maybe finally saving enough for a down payment. But here is the reality check: 1 in 4 of today’s 20-year-olds will experience a disability that keeps them out of work for at least a year before they reach retirement age. According to the Social Security Administration, the risk is much higher than most Millennials realize. Furthermore, a recent LendingTree study found that nearly 52% of Americans don’t have enough in savings to cover a $1,000 emergency. When you combine high risk with low liquid savings, you have a recipe for financial disaster. Disability planning isn’t about being pessimistic; it’s about being unshakeable.

Why Millennials Are the Most Vulnerable Generation?

Millennials often carry a unique set of financial burdens that previous generations didn’t face at the same age. We have record-high student loan debt, a housing market that feels like a moving target, and a gig economy that offers flexibility but zero “safety net.” If you are a freelancer or a 1099 contractor, you don’t have a HR department setting up your short-term disability insurance. You are the HR department.

If an injury or a chronic illness (like long COVID, autoimmune flares, or severe mental health struggles) forced you to stop working for six months, how would you pay your rent? Most Millennials rely entirely on their ability to trade time for money. If that trade stops, the income stops, but the bills—especially the medical ones—actually increase.

The “I’m Healthy” Fallacy

One of the biggest hurdles in disability planning is the “invincibility complex.” We tend to associate disability with catastrophic accidents—car crashes or falls. In reality, the Council for Disability Awareness reports that about 90% of disabilities are caused by illnesses, not accidents. We’re talking about cancer, heart disease, diabetes, and mental health conditions. These don’t care how many green smoothies you drink or how often you hit the gym. Being “healthy” today is the best time to get covered, because insurance companies price your risk based on your current health. If you wait until you have a diagnosis, you’ve waited too long.

The Reality of the Protection Gap

Visualizing the gap between risk and preparation is essential. Many Millennials assume Social Security (SSDI) will catch them, but the approval process is notoriously difficult and the average monthly benefit often falls below the poverty line for a single person.

As shown in the chart above, while the risk is high (52%), the number of young professionals with private, portable disability insurance is shockingly low. Relying solely on an employer-provided plan can also be risky, as those policies often don’t follow you if you switch jobs or start your own business.

Understanding the Two Main Types of Disability Insurance

Not all coverage is created equal. When you start your planning journey, you need to distinguish between Short-Term Disability (STD) and Long-Term Disability (LTD).

Short-Term Disability (STD): This usually covers you for the first 3 to 6 months of an illness or injury. It’s meant to replace a portion of your income (usually 60-80%) while you recover from surgery or a brief illness. Many employers offer this as a standard benefit.

Long-Term Disability (LTD): This is the “big guns” of financial planning. LTD kicks in after your STD or “elimination period” ends. It can pay out for 2 years, 5 years, or even until you reach retirement age (65-67). For Millennials, LTD is the most critical component because it protects your “human capital”—the millions of dollars you are expected to earn over the next 30 years.

Why Your Employer’s Plan Might Not Be Enough

It’s a common relief: “Oh, I have benefits through work.” While that’s a great start, group disability policies have several “gotchas” that Millennials need to look out for:

-

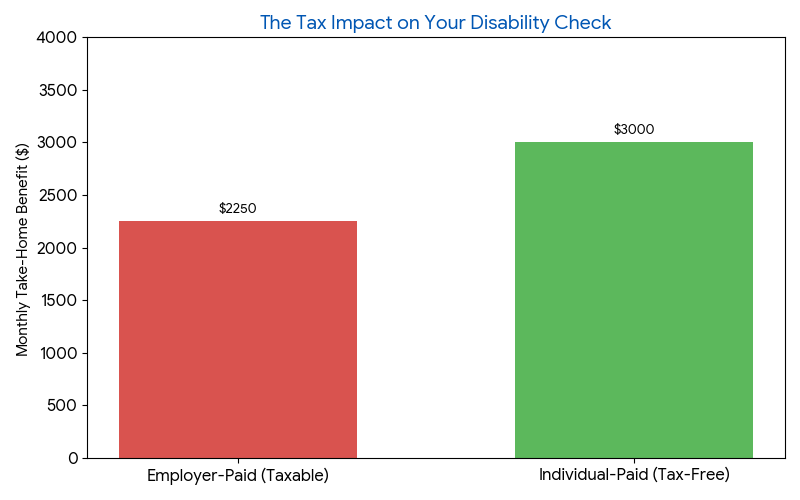

Taxes: If your employer pays the premiums, the benefit you receive is usually taxable. If the policy promises 60% of your income, after taxes, you might only see 40% in your bank account.

-

The “Any Occupation” Trap: Many group plans only pay out if you can’t perform any job. If you’re a surgeon who can no longer operate but could technically work at a call center, an “any occupation” policy might stop paying.

-

Lack of Portability: If you leave your job, you leave your coverage. In an era where Millennials change jobs every 2-3 years, this creates dangerous gaps in protection.

As seen in the chart above, the difference in take-home pay can be substantial. If you pay your own premiums with after-tax dollars, the benefits are typically tax-free.

Deep Dive: Own-Occupation vs. Any-Occupation

This is the most critical distinction in any disability policy. Imagine you are a graphic designer or a software engineer. You spend your day at a desk, using your eyes and your hands.

-

Own-Occupation: If you develop a condition that prevents you from performing the specific duties of a graphic designer, you receive your benefit—even if you are healthy enough to work as a greeter at a local store. This protects your specialized income.

-

Any-Occupation: This is a much stricter standard. To receive benefits, you must be unable to perform any job for which you are reasonably suited by education or experience. If the insurance company decides you can work in a different field (even at a lower pay grade), they can stop your payments.

For Millennials with specialized degrees and high-income potential, “Own-Occupation” is the gold standard.

Case Study: Sarah and the Unforeseen Gap

Sarah is a 32-year-old marketing manager in Chicago. She’s healthy, active, and earns $85,000 a year. She relies on her employer’s group long-term disability plan, which covers 60% of her salary.

In early 2025, Sarah is diagnosed with a severe neurological condition that causes chronic migraines and light sensitivity, making it impossible to stare at a computer screen for more than 15 minutes.

The Crisis: Sarah’s employer-paid benefit kicks in, but because the employer paid the premiums, her $4,250 monthly benefit is taxed. After federal and state taxes, she takes home roughly $3,100. Her rent, student loans, and car payment total $2,800. She has only $300 left for food, utilities, and her new, expensive medical treatments.

The Alternative: If Sarah had supplemented her work plan with a small individual “Own-Occupation” policy, she would have received an additional $1,500 tax-free every month. That “safety layer” would have been the difference between focusing on her recovery and worrying about an eviction notice.

How to Build Your Disability Safety Net: Step-by-Step

Disability planning doesn’t have to happen all at once. You can build it in layers, much like a diversified investment portfolio.

Step 1: The Emergency Fund (The Foundation) Before buying insurance, you need 3-6 months of bare-bones expenses in a high-yield savings account. Most disability policies have an “elimination period” (the waiting time before pay starts) of 90 days. Your savings account is your “bridge” for those three months.

Step 2: Maximize Group Insurance Opt-in to whatever your employer offers. It’s usually the cheapest way to get baseline coverage without a medical exam. If they offer a “buy-up” option to increase your coverage from 50% to 60%, take it.

Step 3: Secure an Individual Policy (The Shield) This is a policy you own. It stays with you if you get fired, quit, or start a business.

Step 4: The Underwriting Process When you apply for an individual policy, you will go through “underwriting.” This typically involves:

-

An application with your medical history.

-

A brief phone interview.

-

Sometimes a “para-med” exam (blood and urine samples).

-

A review of your income (tax returns or W-2s).

Don’t be intimidated! The process ensures that your policy is customized to your exact needs and health profile.

The Cost of Waiting: The “Age Tax”

Every year you wait to lock in a disability policy, the premium goes up. Unlike car insurance, which might go down as you get older and “wiser,” disability insurance only gets more expensive as your body ages. By locking in a “Non-Cancellable” and “Guaranteed Renewable” policy in your 20s or early 30s, you freeze your rates at your healthiest self.

Think of it as a gift to your 50-year-old self. You are essentially buying a contract that says, “I will pay $30 a month now so that if my health fails later, my lifestyle won’t.”

Common Myths That Hold Millennials Back

Myth #1: “I’ll just use Worker’s Comp.” Wrong. Worker’s Compensation only covers injuries that happen on the job. According to industry data, less than 5% of disabling conditions are work-related. If you get cancer or have a stroke at home, Worker’s Comp won’t pay a dime.

Myth #2: “I’m too young to worry about this.” As the stats show, disability is a young person’s risk. You have more years of potential income to lose than a 60-year-old does. Your “income-earning potential” is likely your most valuable asset—even more than your home or your car.

Myth #3: “It’s too expensive.” A basic long-term disability policy usually costs 1% to 3% of your annual income. If you make $70,000, you’re looking at roughly $700 to $2,100 a year—or about the cost of a monthly streaming subscription and a few lattes. Is 2% of your paycheck worth protecting the other 98%?

Mental Health and Disability: The New Frontier

We can’t talk about Millennial disability planning without mentioning mental health. Burnout, clinical depression, and severe anxiety are leading causes of long-term disability claims for our generation.

When shopping for a policy, check the “Mental and Nervous Disorders” provision. Some policies limit these claims to 24 months, while others (premium policies) cover them just like physical illnesses. Given the stressors of modern life, ensuring your policy treats mental health with the same weight as physical health is non-negotiable.

Frequently Asked Questions (FAQ)

Q: Can I get disability insurance if I have a pre-existing condition? A: Yes, but the insurance company may “exclude” that specific condition. For example, if you have a history of back pain, they may cover you for everything except back-related issues. It’s still worth having for the 10,000 other things that could happen.

Q: What if I am a freelancer or part of the “Gig Economy”? A: You are the most at-risk group. Since you have no employer-paid benefits, an individual policy is your only line of defense. Look for policies geared toward “Business Overheads” if you run a small agency.

Q: Does Social Security Disability (SSDI) cover me? A: SSDI is the safety net of last resort. The definition of disability is extremely strict (you must be unable to do any work in the national economy), and the average wait time for an appeal can be over a year. It is not a reliable primary plan for a professional Millennial.

Action Steps You Can Take Today

✅ Check your pay stub: See if you are already paying for STD or LTD.

✅ Read your “Summary Plan Description”: Ask HR for the document that explains your disability benefits. Look for the terms “Own Occupation” vs. “Any Occupation.”

✅ Get a quote: Talk to an independent insurance broker who can compare different private plans. It costs nothing to get a quote.

✅ Audit your expenses: Know exactly how much you need to survive every month. This is your “target benefit” number.

Final Thoughts: Freedom Requires Security

We talk a lot about “financial freedom” in the Millennial community. We want the freedom to travel, the freedom to work remotely, and the freedom to retire early. But true freedom is impossible without security. You aren’t truly free if one bad biopsy or one slick patch of ice could lead to bankruptcy.

Disability planning isn’t just a “boring adult thing.” It’s a foundational act of self-love. It’s telling yourself that your future, your comfort, and your hard work are worth protecting. Start now, while you’re young, healthy, and have the most to gain.

Sources & Data References

-

Social Security Administration (SSA): Disability Benefits Fact Sheet

-

Council for Disability Awareness: Disability Statistics and Causes

-

Bureau of Labor Statistics: Employee Benefits in the United States

-

The Federal Reserve: Report on the Economic Well-Being of U.S. Households