Disclaimer:

The information provided on MyAmericanSavings.us is for educational purposes only and should not be construed as financial, investment, or legal advice. Please consult with a licensed professional before making any financial decisions.

It felt impossible. I remember sitting on my worn-out hand-me-down couch in my cramped apartment, looking at the median home sales price in the United States, which, according to recent Federal Reserve data, has hovered around the $420,000 mark. A 20% down payment on that is $84,000. My bank account balance? Precisely $0.00.

Actually, that’s not true. It was $0 designated for a house. I had an emergency fund, sure, but the idea of accumulating a five- or six-figure sum felt like trying to empty the ocean with a teaspoon.

The American dream felt more like a distant, heavily taxed fantasy. I knew that despite the chatter about 3% or 5% down payment options (which I did explore), the path to financial stability and minimizing PMI (Private Mortgage Insurance) lay in aiming for a substantial down payment.

My dream home required a monumental effort. This is the exact, unvarnished story of how I went from that zero balance to holding the keys to my front door. It wasn’t magic; it was math, sacrifice, and a spreadsheet that became my best friend.

Phase 1: The Cold, Hard Audit

Before I could save, I had to stop the bleeding. I couldn’t just ‘spend less.’ I needed to know exactly where every dollar was going. I committed to a 30-day financial audit that was eye-opening and, frankly, embarrassing.

I am not a fan of complicated budgeting software; I used a simple spreadsheet. I meticulously tracked every single transaction. Every 99-cent app purchase, every streaming service, and, yes, every overpriced coffee.

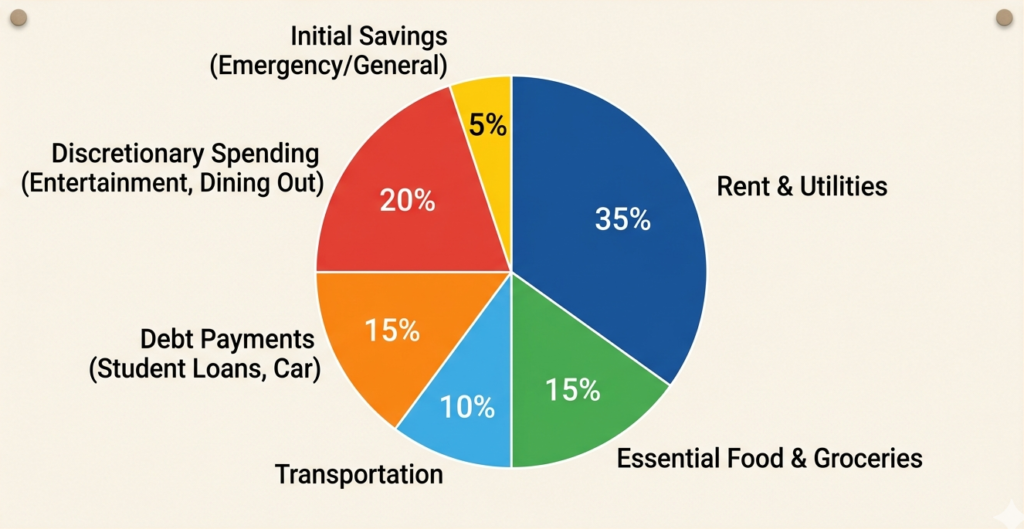

The chart below shows what my spending looked like before I got serious. As you can see, ‘Discretionary Spending’—the stuff I didn’t actually need—was consuming nearly a quarter of my income. This was the first place to look for my down payment money.

My Initial Spending Breakdown (A Reality Check)

The audit taught me three things:

-

I was bleeding money on convenience. Dining out and delivery were huge culprits.

-

Fixed expenses weren’t actually fixed. My phone bill and internet were higher than necessary.

-

My savings habit was non-existent. I saved whatever was ‘left over,’ which was usually near zero.

Phase 2: The Tactical Budget Makeover

I knew I needed a war plan. A basic budget was not going to give me $50,000+ in a reasonable timeframe. I switched to the Zero-Based Budget (ZBB). Every dollar I earned was assigned a job before the month began.

-

Job 1: Housing and Utilities.

-

Job 2: Essential Food and Debt.

-

Job 3: The ‘House Fund.’

-

(Very few remaining jobs): Everything else.

Negotiating and Slicing Fixed Costs

I attacked my recurring bills with a vengeance. I spent hours on the phone.

-

Phone Bill: I switched from a major carrier to a Mobile Virtual Network Operator (MVNO). My bill dropped from $85 to $25 a month. Savings: $720/year.

-

Internet: I called my provider and asked for current promotions. They dropped my monthly rate by $20. Savings: $240/year.

-

Insurance: I shopped around and bundled my renters and auto insurance, saving $30 a month. Savings: $360/year.

Total saved just by making calls: $1,320 annually. That was 1.3% of a huge down payment, found in a few hours of uncomfortable phone calls. It was motivating.

Slicing Discretionary (The Painful Part)

This is where the human element really hurts. I stopped dining out. Entirely. I learned to cook, and I meal-prepped every Sunday. My weekly grocery bill was strictly capped.

I also eliminated subscriptions. I was paying for three streaming services I rarely watched. I cut them all, keeping only a library card for free entertainment (books, movies, even audiobooks).

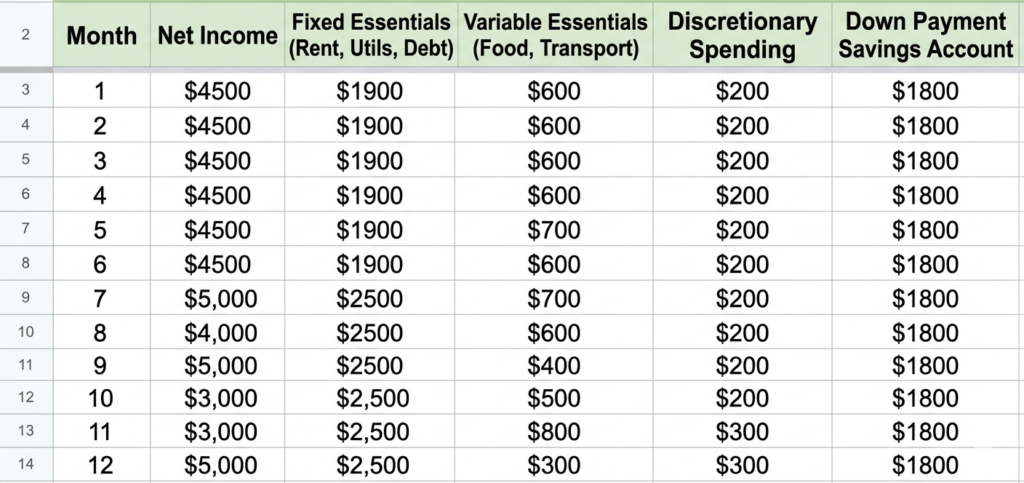

The result of this radical transformation is shown in the image below. This is what my first aggressive year of savings actually looked like on paper. I went from saving $0 specifically for the house to saving $12,700 in one year. Seeing this spreadsheet grow became addictive.

My First Year Savings Blueprint

This blueprint isn’t just a list of numbers—it’s the map of a behavioral shift. In Year One, I moved from “saving what was left” to paying myself first.

1. The “Non-Negotiable” Transfer

The most important column is the Down Payment Savings. I treated this like a mandatory bill. By automating $1,800 to my HYSA the moment I got paid, I forced my lifestyle to adapt to whatever remained. If the money wasn’t in my checking account, I couldn’t spend it.

2. Mastering the “Swing” Months

Budgeting isn’t a straight line. In Month 5, my car needed repairs (Variable Essentials spiked), and in Month 12, I received a bonus (Income spiked).

-

The Rule: When income went up, spending stayed flat.

-

The Result: Every “extra” dollar from tax refunds or bonuses went straight to the house fund, not a lifestyle upgrade.

3. The 5% Sanity Rule

You’ll notice Discretionary Spending never hits $0. I kept about $200–$300 a month for “life”—a movie, a cheap date night, or a hobby. Total deprivation leads to burnout; this small allowance was the “secret sauce” that kept me disciplined for 12 straight months.

Year One Results at a Glance:

-

Total Base Savings: $21,600.

-

Savings Rate: ~40% of my take-home pay.

-

The Win: I proved to myself that I could live on less while watching my future front door get closer every month.

Phase 3: The Growth and Optimizing Momentum

Cutting costs was essential, but I was limited by my income. After a year, the $12,700 was fantastic, but if I wanted to be a homeowner before I was gray, I needed more speed. Phase 3 was about maximizing what I already had and finding ways to generate more.

Maximizing Returns (Safely)

I realized my $12,700 was sitting in a standard checking account, earning a miserable 0.01% interest. That’s essentially letting inflation eat my savings. I needed that money to work.

I immediately moved my growing house fund to a High-Yield Savings Account (HYSA). This is crucial for down payment savings. Your money must be accessible (liquid) but earn a decent return. The national average savings rate is low, but specialized online banks consistently offer rates much, much higher. The interest I earned (compound interest, my friends!) added thousands of dollars over the years, completely passively.

Increasing My Income: The Hustle

The biggest booster to my savings timeline was increasing the amount of money coming in. I was working a full-time job (40 hours/week), but I had weekends and evenings free. I committed to a side hustle.

This is very personal. I didn’t have special freelance skills, so I opted for labor-based gig work. I spent 10–15 hours a week driving for a rideshare app and delivering food. It was exhausting. There were Friday nights I wanted to be out with friends, but instead, I was driving them to their parties. The discipline required cannot be overstated.

The income was variable, but I had one strict rule: 100% of my side hustle income went directly to the HYSA ‘House Fund.’

Windfalls and Automation

I automated everything. My main employer direct-deposited a fixed amount (the maximum I could afford to save from my main budget) directly into the HYSA, bypassing my checking account. If I didn’t see the money, I didn’t miss it.

Furthermore, every ‘windfall’ was committed:

-

Tax refunds? Directly to the HYSA.

-

Annual work performance bonuses? Directly to the HYSA.

-

Cash gifts for birthdays/holidays? Directly to the HYSA.

These windfalls often added $2,000–$4,000 to my annual savings, providing sudden jumps in momentum.

The Mental Game: Staying Sane When You’re Slicing Your Life

This path is difficult. A three-year-plus savings journey is a marathon, not a sprint. The mental fatigue is real. If you don’t build in some ‘release valves,’ you will burn out and blow your savings on a retaliatory vacation.

How I stayed sane:

-

The ‘Guilt-Free Spending’ Category: When I restructured my budget, I gave myself a tiny ‘fun’ fund: $40 a month. It was just enough to see one movie or buy a few fancy coffees. That $40 saved my sanity.

-

Celebrating Small Wins: My spreadsheet was visual proof of progress. When I hit $10,000, I celebrated (with my $40 fund). When I reached $25,000, I celebrated again.

-

The Power of ‘Why’: I wrote down exactly why I wanted a home. I visualized the garden I would plant. The space I would have. I kept that list on my fridge as a constant reminder on the hard days.

Summary of My Multi-Year Down Payment Strategy

This table summarizes my multi-year approach. It was a compounding effect: Year 1 was about discipline, Year 2 was about boosting the growth, and Year 3 was about aggressive optimization.

| Timeline | Milestone Goal | Main Strategy | Visual Progress |

| Year 1 (Discipline) | $0 to $12,000 | Strict 30-day audit. Implemented Zero-Based Budget. Negotiated/cut $1,320 in fixed bills. Switched checking to HYSA. 100% of windfalls saved. | (See Year 1 Savings Blueprint image) |

| Year 2 (The Boost) | $12,000 to $35,000 | Maintained budget. Started side hustle (15 hrs/wk). Automating HYSA transfers. Maximizing HYSA interest rates (e.g., FDIC national rate data). | (See initial spending pie chart transformation) |

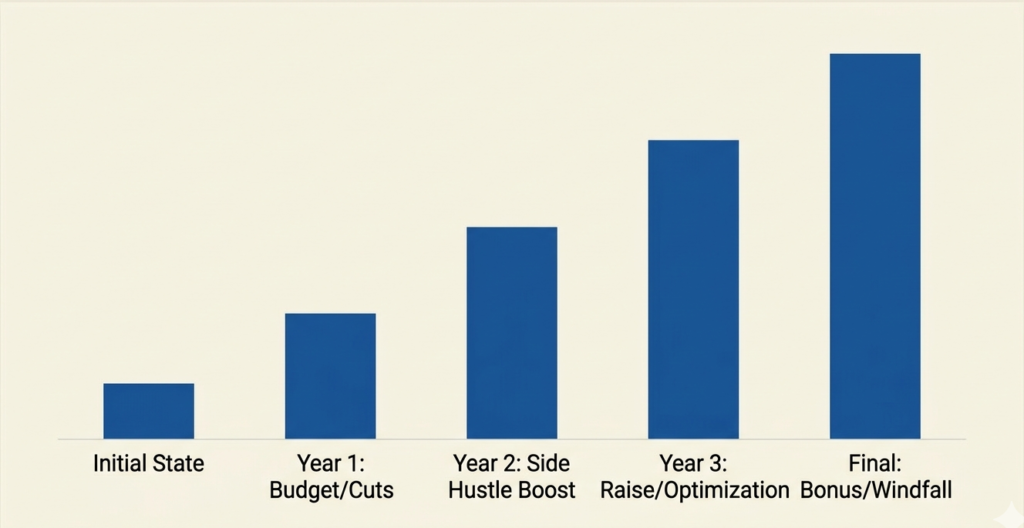

| Year 3 (Maximize) | $35,000 to $65,000+ | Aggressive side hustle. Major career shift (gained a salary increase). 100% of the raise went to savings. | (See final year growth and cumulative savings bar chart, image 3) |

My journey culminated in a massive Year 3, where I combined my optimized budget, increased side hustle income, and a small salary increase. As shown in the graph below, my final push was exponential, finally getting me over that seemingly impossible hurdle.

The Final Stretch: My Cumulative Down Payment Growth

I am not naturally disciplined. I have splurged and made bad financial decisions. But I was motivated by a single, powerful ‘why.’

Saving a massive amount of money from a baseline of $0 is incredibly hard. I cannot promise it will be easy, or that you won’t feel left out when friends go to music festivals you’ve skipped. But if you are tired of paying your landlord’s mortgage and are willing to embrace a season of aggressive math and discipline, this exact strategy can be your roadmap.