Key Points

- Saving for college becomes easier when you follow age-based milestones, helping you stay on track without feeling overwhelmed.

- Starting early allows smaller monthly contributions to grow significantly over time through compounding and consistent saving.

- A successful college fund usually comes from multiple sources like monthly savings, investment growth, bonuses, and side income—not just one stream.

Saving for college is one of those goals that feels both important and overwhelming at the same time. I remember the first time I tried to calculate how much I needed—it felt like staring at a moving target. Tuition keeps rising, living costs add up, and every source seemed to give a different number.

But once I broke it down by age and created a simple plan, everything started to feel manageable.

Let’s start with the reality.

The average cost of college in the U.S. continues to rise. Recent data shows that public in-state colleges cost around $24,920 per year, while private colleges can exceed $58,600 annually, including tuition, housing, and fees.

At the same time, families are shouldering a significant portion of these costs. On average, families pay about 48% of college expenses out of pocket, which equals roughly $13,760 per year.

And here’s something that really stood out to me: even though many parents want to save, only about 56% of U.S. parents are actively saving for college, and many feel they’re behind.

That’s exactly why having a simple, age-based savings plan can make a huge difference.

Related: The Biggest Mistakes Parents Make When Saving for College

Related: The Biggest Mistakes Parents Make When Saving for College

Why Saving by Age Actually Works?

When I first started saving, I made the mistake of thinking I needed a lump sum goal—like $100,000 or more. That felt impossible.

But when I switched to an age-based approach, everything changed.

Instead of asking,

“How much do I need total?”

I started asking,

“How much should I have saved by this year?”

This shift made the process feel:

-

More realistic

-

Easier to track

-

Less overwhelming

Financial planners often use benchmarks based on your child’s age, assuming consistent monthly savings and moderate investment growth.

A Simple College Savings Chart by Age

Below is a simplified version of what a realistic savings path might look like if your goal is to cover about 50% of future college costs (a common strategy).

College Savings Milestones

| Child’s Age | % of Goal Saved | Example Goal ($100K Target) |

|---|---|---|

| 0–2 | 5–10% | $5,000 – $10,000 |

| 3–5 | 15–25% | $15,000 – $25,000 |

| 6–8 | 30–45% | $30,000 – $45,000 |

| 9–11 | 50–65% | $50,000 – $65,000 |

| 12–14 | 70–85% | $70,000 – $85,000 |

| 15–17 | 90–100% | $90,000 – $100,000 |

These benchmarks are based on long-term savings strategies that assume steady contributions and growth over time.

Visual Breakdown: How Savings Grow Over Time

Think of your savings journey like a gradual climb rather than a sprint.

Here’s a simple representation:

Age 0

██████████ 0%

Age 5

██████████ 20%

Age 10

██████████ 50%

Age 15

███████████ 80%

Age 18

███████████ 100%

The biggest takeaway here is that early years matter the most, even if the amounts are small.

What If You Start Late?

I’ll be honest—many people don’t start saving when their child is born. Life gets busy, expenses pile up, and sometimes saving for college just isn’t the priority.

The good news is that starting late doesn’t mean you’ve failed. It just means your strategy needs to adjust.

Example: Starting at Age 10

Let’s say your goal is $80,000 and your child is already 10 years old.

You have about 8 years left.

-

Monthly savings needed: around $600–$700

-

With moderate growth, this is still achievable

Compare that to starting at birth:

-

Monthly savings needed: around $200–$300

This shows how time reduces pressure.

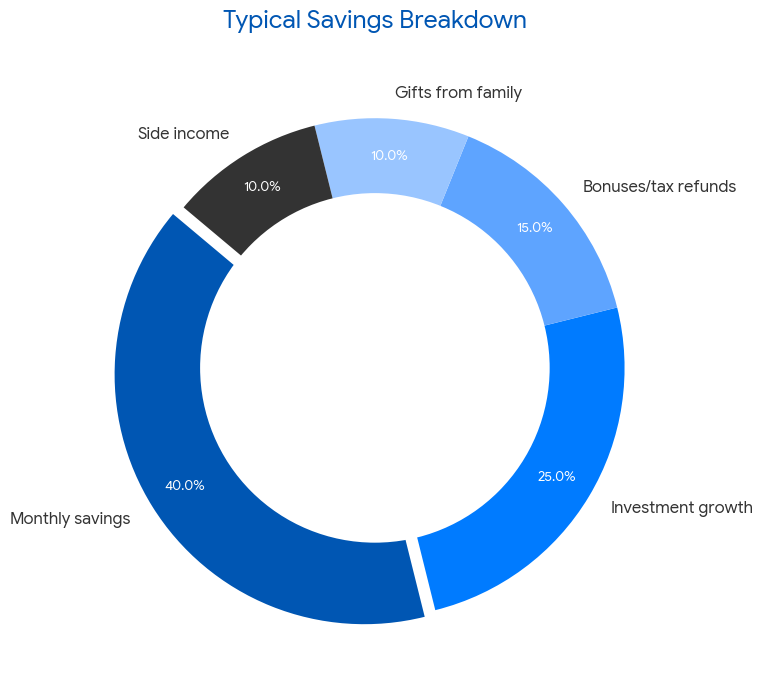

Where the Money Actually Comes From

One of the biggest misconceptions I had was thinking that college savings had to come from one source.

In reality, most families build college funds from multiple streams.

Typical Savings Breakdown (Pie Representation)

If you imagine this as a pie chart, you’ll notice something important:

Savings isn’t just about discipline—it’s also about diversifying how you build your fund!

The biggest takeaway from this chart is simple: You don’t need to rely on just one source to save for college.

Instead, a successful strategy spreads the effort across:

✓ Consistent monthly savings

✓ Long-term investment growth

✓ Occasional financial boosts

✓ Extra income streams

This approach makes the goal feel more achievable because you’re not depending on a single large contribution.

The Role of 529 Plans in College Savings

At some point, I realized I needed a better place to store and grow my savings.

That’s when I learned about 529 plans.

These are tax-advantaged accounts specifically designed for education savings. And they’re more popular than I expected.

-

Over 16 million 529 accounts exist in the U.S.

-

Total savings exceed $500 billion

-

The average account balance is around $30,000

The biggest benefits include:

-

Tax-free growth

-

Tax-free withdrawals for education

-

Flexibility for different education paths

Even small contributions into a 529 plan can grow significantly over time.

Monthly Savings Strategy That Works

Here’s a simple approach I’ve seen work consistently:

Example Monthly Plan

| Contribution Type | Monthly Amount |

|---|---|

| Automatic transfer | $250 |

| Extra savings | $100 |

| Side income | $150 |

Total monthly savings: $500

Over 18 years, with moderate growth, this could reach:

-

$150,000+ in savings

The key here is consistency, not perfection.

Realistic College Savings Targets

One of the most important things I learned is this:

You don’t need to save 100% of college costs.

Many families aim to cover:

-

30%–50% through savings

-

The rest through scholarships, income, or loans

This aligns with real-world data showing that families combine multiple funding sources to pay for college.

Common Mistakes to Avoid

Over time, I’ve noticed a few patterns that can slow down progress:

❌ Waiting Too Long to Start

Even small contributions early on can make a big difference.

❌ Trying to Save Everything

You don’t need to cover the full cost—partial savings still help.

❌ Ignoring Inflation

College costs typically increase over time, so planning ahead matters.

❌ Not Tracking Progress

Without tracking, it’s easy to fall behind without realizing it.

How to Stay Consistent With Saving

Saving for college isn’t just about numbers—it’s about habits.

Here’s what helped me stay consistent:

-

Automating monthly contributions

-

Increasing savings gradually each year

-

Saving windfalls like tax refunds

-

Reviewing progress every 6–12 months

Even small improvements each year can significantly impact your total savings.

A Simple Spreadsheet You Can Follow

Here’s a basic template you can use:

Annual College Savings Tracker

| Year | Total Saved | Goal Progress |

|---|---|---|

| Year 1 | $5,000 | 5% |

| Year 3 | $15,000 | 15% |

| Year 5 | $30,000 | 30% |

| Year 10 | $60,000 | 60% |

| Year 15 | $85,000 | 85% |

| Year 18 | $100,000 | 100% |

This type of tracking makes your progress visible and keeps you motivated.

Key Takeaways for College Savings

Saving for college doesn’t have to feel overwhelming. Once you break it down by age and create a plan, it becomes much more manageable.

-

Start early, even with small amounts

-

Use age-based benchmarks to stay on track

-

Combine multiple savings sources

-

Stay consistent rather than perfect

My Thoughts on Saving for College by Age

If there’s one thing I’ve learned, it’s this: saving for college is less about hitting a perfect number and more about building a system that works for your life.

Whether you’re starting when your child is a newborn or a teenager, there’s always a way forward.

The earlier you start, the easier it gets—but even if you’re starting late, consistent effort can still get you there.

At the end of the day, every dollar saved is one less dollar that needs to be borrowed.

And that alone makes the effort worth it.

Sources