Key Points

- AI budgeting increased monthly savings by $650 in just 30 days by reducing unnecessary spending.

- Real-time tracking and predictions helped control impulse spending and improve financial awareness.

- AI works best as a financial co-pilot, not a replacement—human decisions still matter.

Why I Tried Letting AI Control My Money

If you had told me a year ago that I’d trust artificial intelligence to manage my monthly budget, I would’ve laughed. But here we are in 2026—and things have changed fast.

Recent data shows that about 43% of Americans have already used AI for financial planning, and that number keeps growing as tools become more accessible.

At the same time, 84% of people say they rely on financial apps more than social media, showing how seriously Americans are starting to take their money.

So I decided to test it myself.

For 30 days, I handed over my budget decisions to AI tools. No spreadsheets. No manual tracking. Just automation, insights, and recommendations.

Here’s exactly what happened—good, bad, and surprisingly emotional.

Related: The 48-Hour No-Spend Weekend: A Step-by-Step Guide to Resetting Your Dopamine

Related: The 48-Hour No-Spend Weekend: A Step-by-Step Guide to Resetting Your Dopamine

My Financial Situation Before the Experiment

Before I started, my finances looked like this:

Monthly Income (After Tax): $4,200

Expenses:

- Rent: $1,500

- Groceries: $450

- Eating Out: $320

- Subscriptions: $110

- Transportation: $200

- Miscellaneous: $600

Savings: $300/month (inconsistent)

The problem wasn’t income—it was awareness. I thought I was budgeting, but I was mostly guessing.

The AI Setup: What I Used

I didn’t rely on just one tool. Instead, I combined three approaches:

- AI chatbot for financial advice

- Budgeting app with automation

- Spreadsheet powered by AI prompts

This hybrid setup mimicked what most Americans are actually doing today—mixing tools rather than relying on one platform.

AI automatically:

- Categorized my spending

- Flagged unusual transactions

- Suggested spending limits

- Predicted end-of-month balances

Week 1: The “Reality Check” Phase

The first week felt uncomfortable.

AI analyzed my past 3 months of transactions and gave me a brutally honest breakdown:

📊 Spending Breakdown (AI Generated)

| Category | Budgeted | Actual | Difference |

|---|---|---|---|

| Groceries | $400 | $450 | +$50 |

| Dining Out | $200 | $320 | +$120 |

| Subscriptions | $80 | $110 | +$30 |

| Miscellaneous | $400 | $600 | +$200 |

Biggest shock: I was overspending by nearly $400/month without realizing it.

AI immediately suggested:

- Cut dining out by 30%

- Cancel 2 unused subscriptions

- Set a weekly spending cap

It felt harsh—but accurate.

Week 2: Automation Started Taking Over

By the second week, things got interesting.

Instead of tracking manually, I received daily insights like:

- “You’ve spent 65% of your dining budget in 10 days”

- “At this pace, you will exceed your monthly budget by $280”

This predictive feature changed everything.

Instead of reacting at the end of the month, I adjusted in real time.

📉 Example Adjustment

- Skipped 2 takeout orders → saved $45

- Cancelled one subscription → saved $15/month

It didn’t feel like budgeting. It felt like having a financial coach in my pocket.

Week 3: Behavioral Changes (This Surprised Me)

This is where the real transformation happened.

AI didn’t just track my money—it changed how I felt about spending.

Every time I was about to make a purchase, I started thinking:

“Will this mess up my AI plan?”

That small mental shift reduced impulse spending dramatically.

Interestingly, research shows that overreliance on financial tech can sometimes reduce financial awareness, but in my case, it actually increased mindfulness.

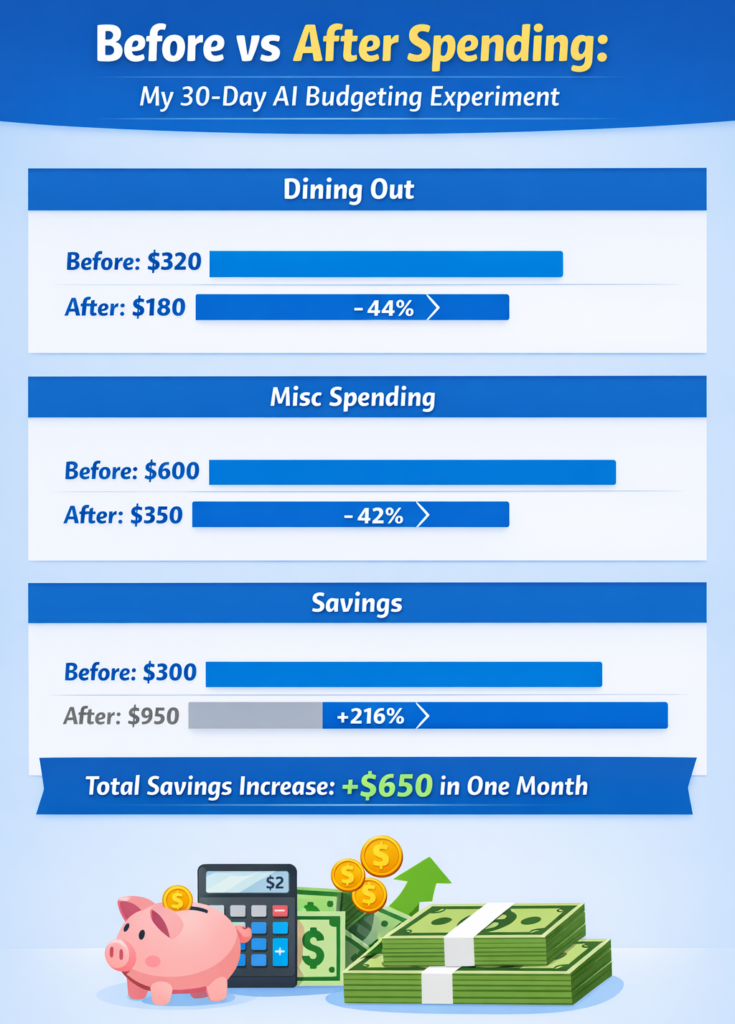

Before vs After Spending

Here’s how my spending changed by week 3:

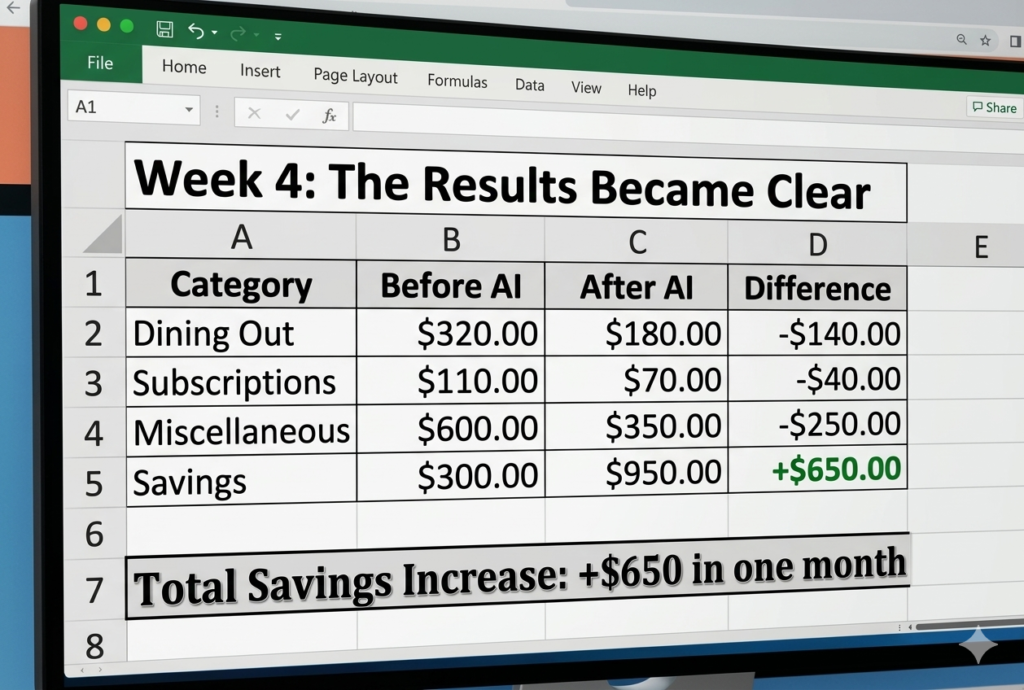

Week 4: The Results Became Clear

By the final week, the numbers spoke for themselves.

📊 Final Monthly Comparison

Total Savings Increase: +$650 in one month

That’s not a small improvement—it’s life-changing for many households.

What AI Did Better Than Me

AI excelled in three areas:

1. Pattern Recognition

It spotted trends I completely missed, like weekend overspending.

2. Consistency

No emotions. No excuses. Just data.

3. Forecasting

It predicted outcomes based on current behavior, which helped me adjust early.

Many companies are now using AI specifically to identify cost reduction opportunities and automate financial decisions, which explains why these tools feel so effective.

Where AI Struggled?

It wasn’t perfect.

1. Context Matters

AI didn’t understand emotional spending.

Example: Buying a birthday gift looked like “overspending.”

2. Over-Optimization

Sometimes it suggested cutting too aggressively, making life feel restrictive.

3. Mistakes Happen

Studies show that over 50% of people who followed AI financial advice made at least one mistake, often due to lack of personalization.

That’s important: AI is a tool—not a decision-maker.

My Real-Life Budget Template (You Can Use This)

Here’s the AI-adjusted budget I ended up with:

📊 Smart Budget Model

| Category | % of Income | Amount |

|---|---|---|

| Needs | 50% | $2,100 |

| Wants | 20% | $840 |

| Savings | 30% | $1,260 |

AI helped me move closer to this ideal structure without forcing it overnight.

The Emotional Side of Letting AI Take Over

This part surprised me the most.

I felt:

- Less stressed about money

- More in control (ironically)

- Less guilty about spending

Why?

Because decisions weren’t random anymore—they were guided.

It removed decision fatigue, which is a huge hidden cost in personal finance.

Would I Keep Using AI for Budgeting?

Yes—but with boundaries.

Here’s how I use it now:

- AI tracks and analyzes

- I make final decisions

Think of it as a co-pilot, not a replacement.

Key Takeaways From My 30-Day Experiment

- AI can significantly increase savings—even in just one month

- Awareness is the biggest financial upgrade, not income

- Automation reduces mistakes and stress

- But blind trust in AI can backfire

My Thoughts: Is AI Budgeting Worth It?

If you’re struggling with:

- Overspending

- Inconsistent savings

- Budgeting fatigue

Then AI can be a powerful starting point.

But the real value isn’t the technology—it’s the behavior change it creates.

In a world where nearly half of Americans are already experimenting with AI for money decisions, ignoring it might actually put you behind.

Sources: