Disclaimer:

The information provided on MyAmericanSavings.us is for educational purposes only and should not be construed as financial, investment, or legal advice. Please consult with a licensed professional before making any financial decisions.

Key Points

- The Psychological Friction Gap: BNPL exploits a cognitive bias by breaking large costs into small, “painless” chunks, which bypasses your brain’s natural resistance to overspending and leads to “payment creep.”

- Regulatory “No Man’s Land”: Unlike credit cards, BNPL services often lack federal consumer protections, meaning you have fewer legal rights regarding merchant disputes, fraud, or faulty products.

- Zero Reward, High Risk: Most BNPL plans won’t help you build your credit score with on-time payments, but they will almost certainly report you to collections and tank your score if you miss even one installment.

We’ve all seen the button at checkout. It pops up right alongside the traditional credit card and PayPal options. A sleek, appealing logo like Affirm, Klarna, Afterpay, or Zip, promising you that you can “Get it now, pay later!” or split your $200 purchase into four easy, “interest-free” payments of $50. In a world where immediate gratification is just a click away, it feels like a financial superpower. It’s no wonder that Buy Now, Pay Later (BNPL) services have exploded in popularity across the United States.

But is this convenient new financial tool truly safe, or is it a debt trap wrapped in slick marketing? As of 2024, approximately 90 million Americans—nearly 35% of the adult population—have used a BNPL service, according to data from The Financial Health Network. This exponential growth is driven by younger consumers; the Consumer Financial Protection Bureau (CFPB) reports that Gen Z and Millennials make up the vast majority of BNPL users. This rapid adoption is occurring despite the fact that, also according to CFPB data, nearly 1 in 5 BNPL users ultimately end up paying late fees or interest. This suggests that while BNPL offers accessibility, it also introduces significant financial risk.

To help you decide if pausing your payment is the right move for your budget, we are breaking down the absolute, non-negotiable risks you must understand before you click “confirm purchase.” We are not just talking about the obvious stuff; we’re diving into the unique, psychological, and systemic traps that make BNPL a unique threat to American financial health.

Related: How to Save Money for Debt Repayment?

Related: How to Save Money for Debt Repayment?

Credit Cards: The Secret to Saving Money (If You Know How to Use Them)

Risk 1: The “Interest-Free” Illusion

The single biggest selling point of BNPL is that it is “interest-free.” And yes, if you follow the “Pay in 4” model perfectly, that can be true. You make the first payment immediately, and the remaining three are auto-deducted every two weeks. If you never miss a payment, you pay exactly the purchase price. But this setup is often just the hook.

Many BNPL providers also offer longer-term financing options for larger purchases (like electronics or furniture). These plans operate much like a traditional personal loan and absolutely do charge interest. Crucially, the Annual Percentage Rate (APR) on these longer-term BNPL loans can be deceptively high—sometimes reaching 30% or more, which is significantly higher than the average credit card interest rate. This isn’t a “Pay in 4”; it’s a high-interest consumer loan disguised in the same slick checkout interface. Failing to distinguish between the simple “Pay in 4” and the “Financing” option is a classic trap.

Risk 2: Late Fees and Penalty Purgatory

The “interest-free” promise is entirely conditional on you being a perfect payer. If you are not perfect, the model shifts dramatically. When you miss a payment, the consequences are immediate and often costly. Most BNPL providers will charge you a flat late fee (often $7–$10) for each missed installment. On a small $50 purchase, a $10 late fee is a massive 20% penalty.

If multiple payments are missed, some services might “roll” that balance into a high-interest loan. But the true danger is what happens next. Unlike a credit card where you can pay a minimum balance to keep your account in good standing, many BNPL “Pay in 4” services do not offer that flexibility. A missed payment means you are in default on that specific loan.

Risk 3: Compulsive Overspending: The Dopamine Trap

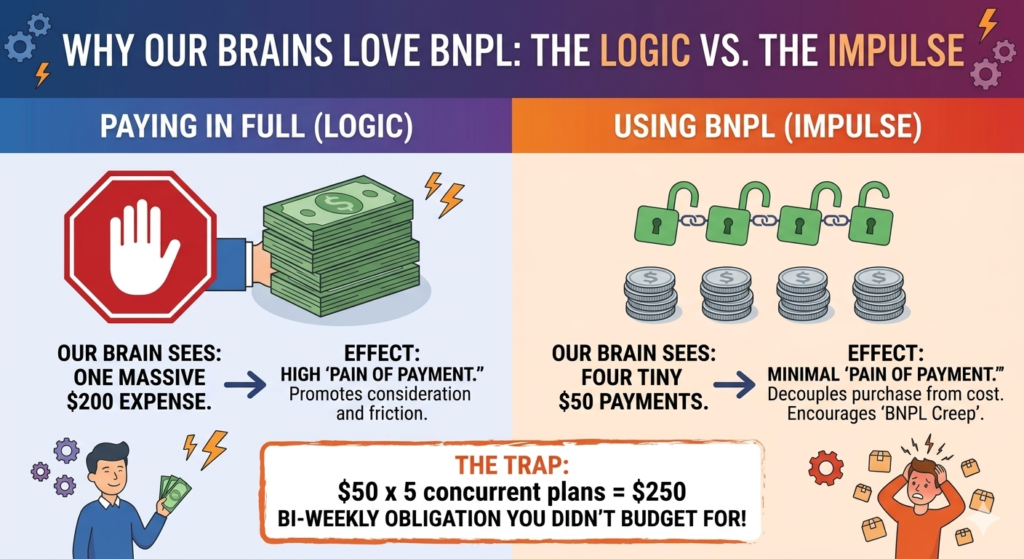

This is the psychological risk that BNPL marketing relies on. BNPL turns a single, painful $200 purchase into four separate, “painless” $50 micro-transactions. The “painless” payment occurs because BNPL breaks a large total into small installments, which tricks the brain into bypassing the “pain of paying” typically felt during a major purchase. By decoupling the immediate gratification of the item from its true cost, it lowers your psychological defense against overspending and impulsive decisions.

A visual showing the “The Psychology of the ‘Painless’ Payment.”

Our brains process these smaller numbers very differently than one large number. We are more likely to justify multiple $50 purchases than one $200 purchase.

Risk 4: Zero Regulation and Phantom Protections

The financial world is split into two halves: highly regulated and everything else. For decades, credit cards have operated under the umbrella of strict U.S. consumer protection laws like the Truth in Lending Act. These laws require clear disclosure of APR, protect you from unauthorized charges, and provide robust dispute resolution processes if an item is faulty or never arrives.

BNPL, because it frequently operates outside the traditional definition of “credit,” is often in the “everything else” category. BNPL loans are technically “point-of-sale installments,” not credit card loans. This means many of the same legal safety nets you take for granted simply do not apply. If you buy a defective laptop using BNPL, the BNPL company is not legally obligated to help you fight the merchant. You owe the BNPL company the full amount regardless of whether the merchant fulfilled their end of the deal.

Risk 5: The Sneaky Impact on Your Credit Score

“Does this affect my credit score?” is one of the most common BNPL questions, and the answer is a complicated, dangerous “it depends.” Most BNPL services will only perform a “soft” credit check to approve you, which does not impact your score. However, they may still report your payment history to credit bureaus, particularly if you misuse the service.

If you are a perfect payer, the service may not report you at all, meaning you receive zero positive benefit for your good behavior. However, if you default on a BNPL loan, that negative mark is almost certain to be reported. A single reported collection from a BNPL service can cause your credit score to plummet by 50 to 100 points, potentially costing you thousands in higher interest rates on future car loans or mortgages. In essence, BNPL offers zero reward for responsible behavior, but severe punishment for irresponsibility.

Risk 6: Dispute Nightmares and Customer “Disservice”

One of the greatest safety features of a major credit card (Visa, Mastercard, Amex, Discover) is their robust customer support and purchase protection guarantees. When you dispute a charge with a credit card, you are dealing with a massive financial institution designed to handle these exact claims. With BNPL, disputes are often a bureaucratic nightmare.

Because BNPL services are fintech startups (or subdivisions of them), their customer service is frequently overwhelmed and under-resourced. Many operate primary support only through AI-powered chatbots or email, making it nearly impossible to speak to a real human. When an item is lost in the mail, you may be caught in a months-long battle where the merchant blames the BNPL company, and the BNPL company blames the merchant, while the payments continue to be auto-deducted from your account.

Risk 7: BNPL Stacking: A Path to Debt Cascades

Stacking is perhaps the most invisible and dangerous behavior associated with BNPL. Traditional lending has guards against this. When you apply for a credit card, the bank sees your entire financial picture and won’t give you $10,000 in new credit if you already have $15,000 in existing debt you can’t manage.

BNPL services operate in isolation. Afterpay doesn’t know (or necessarily care) if you already have three active Klarna plans, two Zip plans, and an Affirm loan. They are only looking at whether your “soft check” passes their minimum approval criteria. This allows a user to “stack” multiple, simultaneously active BNPL loans across different providers. It is dangerously easy for a consumer to accrue $1,500 in total “active” BNPL debt, spread across five different services, all without any central system alerting them that they are in over their head. When one “Pay in 4” payment inevitably bounces, it can trigger a cascade of NSF (non-sufficient funds) fees that devastate an entire bank account.

Risk 8: Hard Inquiries on Long-Term Financing

As mentioned in Risk 1, BNPL providers often offer longer-term financing for larger-ticket items. This “financing” or “monthly payments” option is not a simple “Pay in 4”; it is a formal loan. To approve you for this kind of credit, BNPL services will almost certainly perform a “hard” pull on your credit report.

Unlike soft pulls, hard inquiries are reported on your credit file and will stay there for two years. A hard pull will temporarily lower your credit score by a few points. While one hard inquiry isn’t a disaster, multiple hard pulls—say, from applying for financing on a new TV and a new sofa through two different BNPL services in the same month—will start to significantly impact your score. It also signals to other lenders that you are “desperate” for credit.

Risk 9: The Debt Collection Trapdoor

The true end-of-the-road danger with BNPL is debt collection. Unlike a credit card provider that may work with you to lower payments or manage a hardship, BNPL providers frequently operate with very thin margins and have zero patience for default.

If you miss payments on a “Pay in 4” loan and do not respond to their internal attempts to collect the balance (often with automated emails and texts), they will quickly charge off the debt. This means they sell your “delinquent” account to a third-party debt collection agency for pennies on the dollar. These are professional collection agencies known for persistent phone calls and letters. Once the debt is in collections, it is guaranteed to show up as a collection on your credit report, doing profound and long-lasting damage to your financial reputation.

Risk 10: Incompatible with Financial Planning

This final risk is a structural one. BNPL, by design, is an opportunistic, impulsive financial tool. It is designed to get you to spend money you don’t have right now on an item you probably don’t need. It completely subverts the core tenets of sound financial planning.

A healthy financial plan is based on budgeting: you know exactly how much money is coming in, you have planned for your necessities, you are prioritizing savings, and you have set aside a specific amount for “discretionary” spending. BNPL operates outside of this framework. By making a purchase through BNPL, you have now obligated your future income to pay for a past impulsive decision. You are now paying $50 this month, $50 next month, and $50 the following month for a dress you bought on a whim. This completely cannibalizes your discretionary income for the next three months, making it impossible to stick to a future budget.

Safety is in the Eyes (and the Wallet) of the Beholder

So, is Buy Now, Pay Later safe? The honest, nuanced answer is “No, it is not inherently safe.” It is a financial tool that, when misused, has a catastrophic potential for consumer harm. It relies on psychological triggers, operates with minimal regulation, and offers a deceptively simple path to unmanageable debt.

However, can it be used safely? Yes, in the same way that a chainsaw can be used safely. If you have the extreme discipline to use it only for planned, necessary purchases, if you are 100% certain you can make every single payment, and if you never use it to buy more than you can afford in cash right now, it can be a convenient cash-flow management tool.

But for the vast majority of consumers, particularly in the United States where debt culture is pervasive and financial literacy is low, the risks far outweigh the rewards. If your primary motivation for using BNPL is “pawsing” the payment because you can’t afford the item today, that is the single biggest red flag you could possibly see. That simple act of postponing payment is not a financial “life hack”; it is a dangerous bet against your own future financial health.

Sources