Disclaimer:

The information provided on MyAmericanSavings.us is for educational purposes only and should not be construed as financial, investment, or legal advice. Please consult with a licensed professional before making any financial decisions.

Key Points

- Expect High Startup Costs: The first year is the most expensive, often exceeding $1,500–$4,500 due to essential “setup” gear and one-time medical procedures like vaccinations and neutering.

- Plan for Emergencies: With 1 in 3 pets needing emergency care annually, you must choose between a monthly pet insurance premium or a dedicated $3,000+ emergency savings fund.

- Budget for “Hidden” Fees: Monthly expenses go beyond food; you must factor in recurring American lifestyle costs like pet rent, local licensing, and travel boarding.

There are few moments in life as purely joyful as bringing a new puppy home. That distinct “new puppy smell,” the clumsy waddles, and the soft whimpers as they curl up on your lap create an intoxicating mix of cuteness that melts even the hardest hearts. But as any veteran pet parent will tell you, those adorable whimpers are frequently accompanied by the sound of cash leaving your wallet. We love them like family, and because they are family, we want to give them the best. In the United States, that commitment comes with a significant price tag, particularly in the first twelve months of their life.

According to recent 2026 industry data from Insurify, the average U.S. dog owner now spends between $1,200 and $4,300 annually on their companion. For a puppy’s first year, these costs often lean toward the higher end—or even exceed $6,000 according to Rover’s cost analysis—due to one-time requirements like spaying or neutering. In fact, research highlighted by Forbes Advisor shows that nearly 1 in 3 pets will require emergency veterinary treatment every year.

The key to enjoying this new chapter without financial stress is preparation. This isn’t about discouraging you from getting a puppy; it’s about empowering you to build a sustainable budget that ensures your new best friend gets everything they need, from their first checkup to their first birthday cake. This checklist will guide you through the initial “Welcome Home” investment, the critical medical essentials, and the lifestyle choices that define your monthly spending.

A Graphical Summary of First-Year Costs

To give you a visual representation of how your money is likely to be distributed in that first year, consider the following breakdown of a typical “Puppy Budget.”

As you can see, medical care and food make up the lion’s share of your expenses. By focusing your savings efforts on these two categories—perhaps by choosing a healthy breed and buying food in bulk—you can significantly impact your overall financial health.

Related: How to Start a Pet Emergency Fund Before the Unexpected Vet Bill Arrives

Related: How to Start a Pet Emergency Fund Before the Unexpected Vet Bill Arrives

From Poodles to Persians: Why Breed Matters When Choosing a Policy

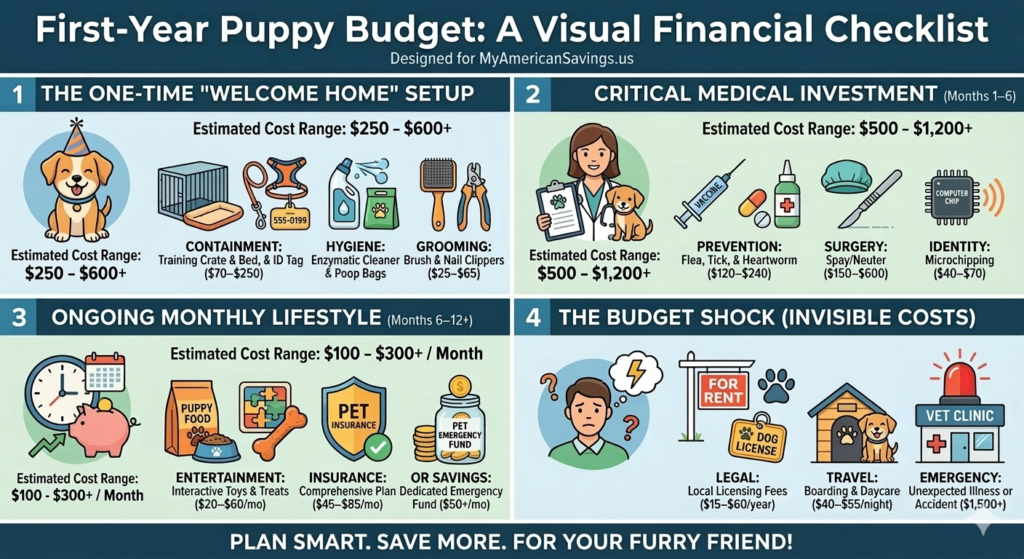

Phase 1: The “Welcome Home” Kit (Month 1 Upfront Costs)

The first few days with your puppy are a whirlwind. You’re sleep-deprived, you’re constantly checking if they’re breathing, and you’re probably cleaning up more messes than you anticipated. This is also when you’ll make your biggest initial investment in “gear.” It’s easy to get carried away in the pet store, buying every cute toy you see, but focus on the essentials first to keep your initial budget under control.

Your primary focus should be on safety, comfort, and containment. Your puppy needs a safe space of their own, which is where a crate becomes invaluable for housetraining and security. Along with the crate, you’ll need durable bowls for food and water, a comfortable bed, and essential walking gear: a high-quality, adjustable collar or harness and a sturdy leash. Remember to get an ID tag with your phone number engraved immediately; it’s a tiny investment that provides immense peace of mind.

Don’t forget the unglamorous essentials. You will need grooming tools appropriate for their specific coat type, an effective enzymatic cleaner for accidents, and a massive supply of poop bags. You might also need to pet-proof your home, which often means investing in baby gates to block off stairs or rooms. While these items represent a significant upfront cost, most are durable goods that will last for years.

| Essential Item | Estimated Upfront Cost (US) |

| Durable Training Crate | $45 – $130 |

| Collar, Leash, Harness & ID Tag | $35 – $85 |

| Stainless Steel Food & Water Bowls | $15 – $45 |

| Orthopedic or Basic Puppy Bed | $25 – $110 |

| Interactive Toys & Teething Chews | $40 – $80 |

| Grooming Kit (Brushes, Clippers) | $25 – $65 |

| Cleanup Supplies (Enzymatic Cleaner) | $20 – $55 |

| Total Estimated Initial Investment | **$205 – $570+** |

Phase 2: The Medical Essentials (Months 1-6)

This is the most critical phase of puppy ownership, focusing on building their immune system and preventing long-term health issues. You will be visiting the veterinarian frequently during the first six months. This is non-negotiable care, and it needs to be a prioritized line item in your budget from day one.

First, your puppy needs a series of core vaccinations, such as DHPP (Distemper, Hepatitis, Parvovirus, and Parainfluenza) and Rabies, to protect them from deadly diseases. These are typically given in boosters every few weeks until they are about four months old. Depending on your location, your vet may also recommend “non-core” vaccines like Bordetella (for kennel cough) or Lyme disease prevention. Along with shots, you’ll need to start them on monthly flea, tick, and heartworm preventatives. Heartworm, in particular, is a devastating disease that is costly to treat but very affordable to prevent.

Another significant cost during this period is the spay or neuter surgery. While adoption fees from shelters often cover this, if you purchase from a breeder or receive a puppy as a gift, you are responsible for the cost. Prices vary widely based on your location and the size of your dog. A private vet clinic may charge $250–$650, while low-cost community clinics might offer the service for $75–$200. Microchipping, which provides a permanent form of identification, is often done at the time of this surgery and is another crucial safety measure for any American pet parent.

Phase 3: The Monthly Lifecycle (Months 1-12 and Beyond)

Once you’ve navigated the initial setup and the heavy medical requirements of the first half-year, your puppy’s budget will settle into a more predictable monthly rhythm. These are the recurring costs of “maintenance”—the things that keep them fed, entertained, and well-behaved as they grow into adulthood.

Food is the most obvious monthly expense. The cost here is highly variable, depending on the size of your puppy and the quality of food you choose. A small breed might cost $30–$50 a month to feed, while a giant breed could easily cost $80–$120 or more. Discussing diet with your veterinarian is essential, as proper puppy nutrition sets the foundation for their lifetime health. High-quality food may have a higher upfront cost but could save you money on vet bills later by preventing nutritional deficiencies or obesity-related issues.

The other major lifestyle variable is training and socialization. A well-mannered dog is a joy to live with; an untrained dog is a source of constant stress and potential liability. Investing in a group puppy obedience class, which typically runs $150–$350 for a multi-week session, is one of the best investments you can make. Beyond formal classes, you’ll need a steady budget for training treats and replacement toys. Puppies chew—a lot—and providing them with appropriate chew toys isn’t just about fun; it’s about protecting your furniture and your sanity.

Phase 4: Navigating the “Invisible” Costs of Living

Many new owners are blindsided by costs that don’t involve a trip to the pet store or the vet. If you live in a rental property, for example, you may face “pet rent” or an additional pet deposit. Across the U.S., pet rent typically averages $35 per month, which adds over $400 to your annual housing costs. Some landlords also require a one-time non-refundable pet fee that can range from $200 to $500.

Then there is the matter of legal compliance. Most municipalities in the United States require you to register your dog and pay for an annual license. These fees are usually modest—ranging from $15 to $60—but they are mandatory and often require proof of rabies vaccination. If you plan to travel, you also need to factor in the cost of boarding or pet sitting. In 2026, the national average for overnight dog boarding is approximately $45 to $55 per night. For a week-long vacation, you could easily spend $350 just on your puppy’s accommodations.

If you work long hours, you might also consider doggy daycare to ensure your puppy gets socialized and exercised. Daycare rates generally fall between $25 and $40 per day. While not every owner needs these services, failing to account for them in your initial budget can lead to a “sticker shock” that strains your monthly finances.

Phase 5: The Pet Insurance vs. Savings Debate

This is where reality can get very expensive, very quickly. While you can budget for the predictable things—food, shots, and toys—you cannot predict an accident or an illness. Your puppy might swallow a rogue sock (creating a surgical emergency costing thousands), develop a sudden allergy, or pick up a stubborn ear infection. These unexpected emergency vet bills are the single biggest threat to a pet owner’s financial stability.

You have two primary strategies to prepare for this:

-

Comprehensive Pet Insurance: This operates similarly to human health insurance. You pay a monthly premium—averaging around $65 for dogs in the U.S. in 2026—and the provider reimburses a significant portion of your bill (usually 70% to 90%) after you meet your deductible. This is the best way to guard against catastrophic, multi-thousand-dollar costs. The key is to enroll your puppy as early as possible before they develop any “pre-existing conditions” that would be excluded from coverage.

-

A Dedicated Pet Savings Fund: If you choose to “self-insure,” you must have a dedicated, liquid savings account. This isn’t a general “rainy day” fund; it is specifically for your pet’s medical emergencies. Financial experts recommend building this fund to at least $3,000 to $5,000 as quickly as possible. This approach requires extreme discipline, as one major surgery can completely wipe out years of savings in a single afternoon.

Phase 6: DIY Strategies to Offset Costs

While the costs of a puppy are high, there are several ways to be a “frugal” pet parent without sacrificing the quality of care. One of the most effective ways to save is through DIY grooming. Professional grooming for a medium-sized dog can cost $60 to $100 per session. By investing $50 in a good pair of clippers and learning to trim their nails and clean their ears at home, you can save over $600 a year.

Another area for savings is home-made treats. Many premium dog treats are expensive and filled with preservatives. Simple recipes using peanut butter, pumpkin puree, and oats can be made in bulk for a fraction of the price of store-bought alternatives. Additionally, buying your preventative medications (flea, tick, and heartworm) in six-month or twelve-month supplies often triggers significant discounts or “buy some, get some” rebates that aren’t available for single-month purchases.

Socialization can also be done for free. Instead of daily daycare, look for local “puppy playdate” groups in your neighborhood or at local parks. These provide the same socialization benefits as paid daycare without the daily fee. However, always ensure your puppy is fully vaccinated before engaging in these public social activities to avoid costly illnesses.

Final Step: Love and Budgeting

Bringing a puppy into your life is a fifteen-year commitment, and the first year is the boot camp. It’s a test of your patience, your sleep schedule, and your budgeting skills. But every dollar you spend on quality food, preventative medicine, and training isn’t just an expense; it’s an investment in a happy, healthy companion who will pay you back in ways that aren’t measurable in currency.

By using this checklist, you’re taking the first steps of responsible pet parenthood. You’re acknowledging that while love is abundant, the reality of vet care, housing fees, and security requires a financial plan. At My American Savings, we believe that financial peace of mind allows you to be a better pet owner. Preparation is the bridge that allows you to move past financial worry and focus on what really matters: teaching your puppy to fetch, watching them discover the world, and enjoying the unconditional love of your new best friend.

Sources:

-

Pet Ownership Costs: Insurify: The Annual Cost of Owning a Dog (2026 Data)

-

First-Year Puppy Budget: Rover: The Cost of Dog Parenthood in 2025/2026

-

Emergency Care Statistics: Forbes Advisor: Pet Insurance Statistics & Facts

-

Average Veterinary Costs: Pawlicy Advisor: How Much Does a Vet Visit Cost? (2025/2026 National Average)

-

Industry Trends: NAPHIA: State of the Pet Health Insurance Industry Report