Disclaimer:

The information provided on MyAmericanSavings.us is for educational purposes only and does not constitute professional financial, investment, or legal advice. Please consult with a licensed professional before making any financial decisions.

Key Points

Look Beyond the Sign-Up Bonus

A large welcome bonus is tempting, but always compare it against the spending requirement, annual fee, and ongoing rewards structure before applying.Compare the APR and Fees Carefully

Interest rates, balance transfer fees, foreign transaction fees, and annual charges can quickly outweigh rewards if you carry a balance.Match the Card to Your Spending Habits

The best card is one that aligns with your real-life expenses — groceries, gas, dining, travel — not one with flashy perks you won’t use.Understand the Fine Print and Long-Term Value

Introductory 0% APR periods, reward expiration rules, and penalty APR clauses can significantly impact whether the offer benefits you over time.

Credit cards can be powerful financial tools, offering convenience, security, and rewards — but they can also lead to costly debt if not chosen carefully. In the United States, credit card usage and debt levels make it critical for consumers to evaluate offers strategically. According to the Federal Reserve Bank of New York, credit card balances climbed to an all-time high of $1.28 trillion in the fourth quarter of 2025, signaling that revolving consumer debt has now surged well past the $1 trillion threshold.

With thousands of credit card products available — each promising rewards, 0% offers, and exclusive perks — consumers must understand which features actually deliver value vs. those that are marketing smoke and mirrors. This guide will walk you through exactly how to evaluate credit card offers, understand the fine print, and make decisions that strengthen your financial health instead of costing you money.

📊 Credit Card Trends at a Glance

| 📌 Metric | 📊 Latest U.S. Data | 💡 What It Means |

|---|---|---|

| 💳 Total revolving credit | $1 trillion+ | Americans carry large credit card balances |

| 📈 Avg. credit card APR | 20%+ | Interest charges are expensive for unpaid balances |

| 🎯 % of cardholders with rewards | ~70%+ | Most cards offer some type of rewards |

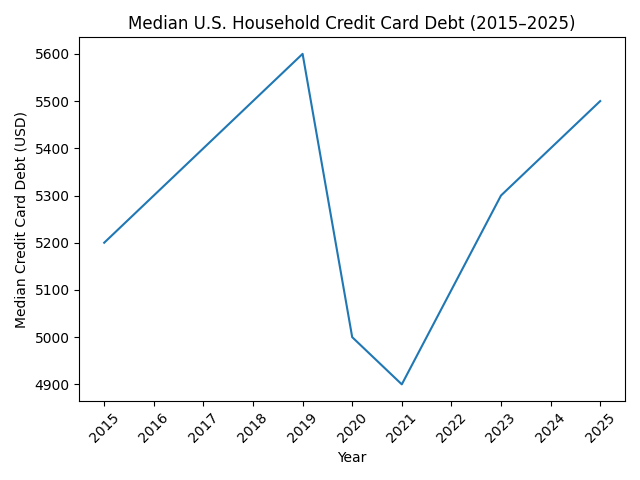

| 🪙 Median household credit card debt | $5,300 | Average unpaid balance per U.S. household |

(Sources: Federal Reserve, FRB of New York — consumer credit reports)

💡 Why Evaluating Credit Card Offers Matters

Too often, consumers apply for credit cards based purely on attractive marketing — flashy reward rates, big sign-up bonuses, or “0% APR” offers — without understanding whether the offer fits their actual financial behavior. That can lead to:

✔ Paying high interest on balances

✔ Missing out on rewards you never use

✔ Paying annual fees for perks you don’t want

✔ Damaging your credit score

Good credit card utilization and choices can improve your financial flexibility and even boost your credit standing. The key is knowing which offers are worth your time and which are disguised traps.

🧠 How to Tell if a Credit Card Offer Is Worth It

The best way to evaluate a credit card offer is to break it down into core components that affect your wallet. Let’s walk through them.

📌 1. Annual Percentage Rate (APR) — The Cost of Carrying a Balance

| 📉 APR Type | 📌 Typical Range | 💡 What It Means |

|---|---|---|

| 💳 Regular Purchase APR | 15%–25%+ | Interest charged when you carry a balance |

| 🪄 Intro 0% APR | 0% (limited months) | Temporary interest relief on purchases or balances |

| 📊 Penalty APR | 29%+ | Activated by late payments — costly |

How to Evaluate APR

If you pay your balance in full every month, APR isn’t as critical because you won’t incur interest charges. However, most U.S. consumers carry balances at least part of the time. If you think you may carry a balance, a lower ongoing APR becomes much more valuable.

👉 Pro tip: If an offer advertises “0% APR” for 12–18 months, calculate how much you’ll save only if you plan to pay down that balance within the promo period. After that period ends, the APR may jump steeply.

📌 2. Rewards & Sign-Up Bonuses — Are They Truly Valuable?

This is where many card offers shine in advertising — big cash-back percentages or massive points bonuses just for signing up.

| 🎁 Reward Type | 📊 Example Offer | 💡 Best For |

|---|---|---|

| 🛍️ Cash Back | 3% on groceries | Everyday spenders |

| ✈️ Travel Points | 60,000 points after $4,000 spend | Frequent travelers |

| 🧾 Tiered Rewards | 1–5% on categories | Category spenders |

| 📆 Intro Bonus | $200–$500 after spending | Short-term spenders |

How to Evaluate Rewards

Ask yourself:

✔ Do I spend enough in the bonus category to earn it?

✔ Do I shop in categories where the card rewards are strong?

✔ Are the redemption options flexible (cash vs travel)?

The highest reward rate doesn’t always mean the best value — especially if it requires spending more than you ordinarily would.

📌 3. Annual Fees — Are the Perks Worth It?

Some cards charge annual fees ranging from $0 to $550+ per year. These fees are common on travel or premium rewards cards.

| 💳 Fee Level | 📊 Examples | 💡 Who It Fits |

|---|---|---|

| 🆓 $0 Annual Fee | Basic cash-back cards | Budget-oriented |

| 💵 $95–$195 | Mid-tier rewards | Regular users of rewards |

| 💎 $450+ | Premium travel cards | Frequent travelers |

When an Annual Fee Might Be Worth It

An annual fee can be worth paying if the card’s benefits outweigh the cost. Look for value drivers like:

-

Annual travel credits

-

Airline/hotel fee credits

-

Priority boarding or lounge access

-

Free Global Entry/TSA PreCheck credits

If your subscription costs more than the rewards you earn, you’re losing money.

📌 4. Intro Offers — 0% APR or Big Sign-Up Bonuses

Introductory offers are powerful anchors in credit card advertising. Common examples include:

-

0% APR for 12–18 months on purchases or balance transfer

-

Bonus rewards points or cash back after spending a set amount in the first 3–6 months

How to Evaluate Them

✔ Read the fine print — introductory perks revert to standard terms after the period ends.

✔ Know your spending pattern — don’t overspend just to earn a bonus.

✔ If you carry debt, 0% APR offers can help consolidate balances only if fees are low.

A 0% APR offer is valuable only if you commit to paying down the balance before the promo ends.

📌 5. Fees & Penalty Charges — Sneaky Costs to Watch

Credit card fees go beyond annual charges. Some common ones include:

| 🧾 Fee Type | 📌 Typical Cost | 💡 When It Applies |

|---|---|---|

| 💰 Late Fee | $30–$40 | Missed payment |

| 💳 Foreign Transaction Fee | 2–3% | Purchases abroad |

| 🔁 Balance Transfer Fee | 3–5% | Transferring debt |

| 🔄 Cash Advance Fee | 5%+ | Withdrawing cash |

Why Fees Matter

Cards with low or no rewards but high fees can still cost you. Conversely, a good rewards card with fees may still be worth it if the perks outweigh the fees. Always calculate your net benefit.

📊 Rewards Value Calculator

Here’s a quick way to estimate whether a rewards offer is worth it:

| 💡 Category | ✍️ Example | 🧮 Estimated Value |

|---|---|---|

| Annual spending | $12,000 | — |

| Reward rate | 2% cash back | $240/year |

| Annual fee | $95 | — |

| Net savings | $145 | Positive ROI |

If your rewards minus fees still leave you with savings, the card can be worth it.

🧠 6. Credit Score Impact — What You Should Know

Applying for new credit triggers a hard inquiry on your credit report, which may temporarily lower your score. Too many inquiries in a short period can give lenders the impression of risk.

However, responsibly opening new accounts — and keeping older accounts open — can improve your credit utilization ratio, which boosts scores over time.

📌 7. Redemption Flexibility — How You Use Rewards Matters

Not all rewards are created equal. Redemption options include:

-

Statement credits

-

Cash back deposited

-

Travel bookings

-

Gift cards

-

Merchandise

Some travel reward programs offer higher value when redeemed for flights vs. statement credits. If points are only redeemable for low-value merchandise, the rewards may be less impressive than they appear.

🧠 8. Perks & Benefits — More Than Just Rewards

Beyond rewards and interest rates, many cards include perks such as:

✔ Travel insurance

✔ Purchase protection

✔ Extended warranties

✔ Rental car coverage

✔ Airport lounge access

These extras provide real value — especially if you were already paying for similar services separately.

📌 How to Compare Two Offers Side-by-Side

Here’s a quick visual way to compare credit cards:

| 🔍 Feature | 🪪 Card A | 🪪 Card B |

|---|---|---|

| APR | 0% Intro → 18.99% | 15.99% |

| Rewards | 3% groceries | 2% all purchases |

| Annual fee | $0 | $95 |

| Sign-up bonus | $200 after $1,000 spend | 30,000 points |

| Foreign fee | Yes | No |

| Best For | Short-term payoff | Frequent travelers |

Comparing like this helps you see which card actually fits your goals rather than chasing shiny headlines.

🧠 Real Life Scenarios: Which Card Makes Sense?

🏠 Scenario 1: You Carry a Balance

Low ongoing APR or 0% introductory offers matter more than rewards here.

✈ Scenario 2: You Travel Often

Rewards, foreign fee waivers, and travel perks provide real value — even with a modest annual fee.

🛍 Scenario 3: Everyday Spender

Cash back on everyday purchases (groceries, gas) helps your budget immediately.

📌 Red Flags: When a Card Offer Might Be a Trap

Watch out for:

❌ Very high APR after intro offers

❌ Rewards that are hard to redeem

❌ High fees with limited benefits

❌ Tempting bonuses that require spending beyond your means

If you have to overspend just to earn a bonus, the card may cost you more than it saves.

🧠 Final Checklist Before You Apply

✔ Do I understand the APR and fees?

✔ Is the rewards structure aligned with my spending?

✔ Can I realistically earn the sign-up bonus?

✔ Are the perks meaningful to me?

✔ Will this impact my credit score negatively?

If you can confidently answer “yes” to these, the offer may be worth pursuing.

📊 Summary Table: Worth It or Not?

| 🔎 Factor | 👍 Positive Indicator | 👎 Negative Indicator |

|---|---|---|

| APR | Low ongoing APR | High APR after intro |

| Rewards | Cash back you’ll use | Complicated point systems |

| Fees | Fees offset by benefits | Fees outweigh rewards |

| Perks | Useful travel/insurance | Perks you won’t use |

🎯 Swipe Smart

Credit card offers aren’t inherently good or bad — what matters is whether they fit your financial behavior and goals. A great card for one person might be a financial trap for another. By understanding interest rates, fees, reward mechanics, and redemption options, you can ensure your next credit card adds value to your financial life instead of costs.

Swipe smart — your wallet and credit score will thank you.