Disclaimer:

The information provided on MyAmericanSavings.us is for educational purposes only and should not be construed as financial, investment, or legal advice. Please consult with a licensed professional before making any financial decisions.

Key Points

- Starting late can significantly increase the financial burden. Early savings benefit from long-term compound growth.

- Ignoring tax-advantaged savings options can reduce potential savings. Accounts like a 529 college savings plan help grow funds efficiently.

- Underestimating total college costs can derail financial plans. Plan for tuition, housing, books, and other living expenses.

Saving for a child’s college education is one of the biggest financial goals many families set. Higher education can open doors to career opportunities, but it also comes with rising costs that require careful planning.

According to 2025 research, the average family spends about $30,837 per year on college expenses, including tuition, housing, and books.

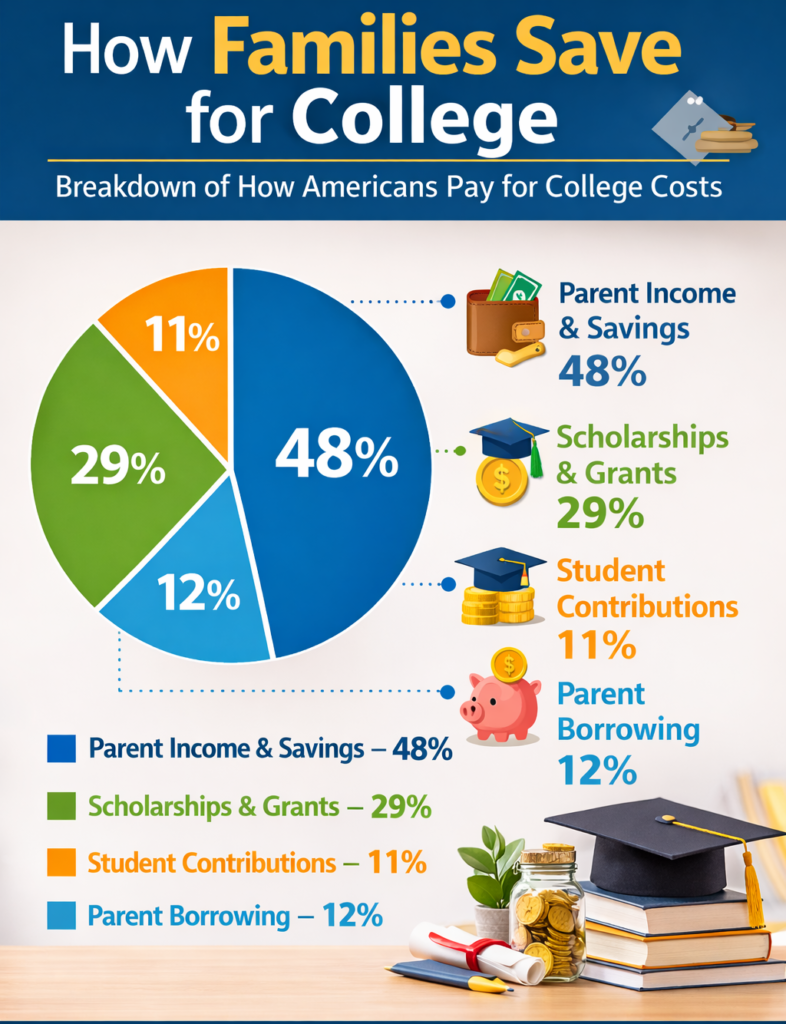

At the same time, parents’ income and savings cover nearly 48% of college costs, making family financial planning a critical part of paying for higher education.

Even though many parents prioritize college savings, there is often a gap between expectations and reality. A Forbes study show that while 74% of parents are saving for college, their savings may only cover about 30% of expected costs.

This gap often happens because families unknowingly make financial mistakes when planning for education expenses. Understanding these mistakes can help parents build a stronger savings strategy and reduce future financial stress.

Below are some of the most common mistakes parents make when saving for college—and how to avoid them.

Related: My Journey Building a College Fund for My Kids From Scratch

Related: My Journey Building a College Fund for My Kids From Scratch

The $100-a-Month College Plan: How Small Savings Can Turn Into Big Tuition Money

The Rising Cost of College And How Families Can Save?

Before looking at common mistakes, it helps to understand why college planning has become more important.

The cost of higher education has steadily increased over the years. A single year at a public in-state university now averages around $24,920, while private colleges can exceed $58,600 per year when tuition, housing, and other expenses are included.

With costs rising faster than many families’ savings rates, planning ahead becomes essential. Parents who start saving early can benefit from compound growth and reduce the amount their children may need to borrow through student loans.

However, without the right strategy, even well-intentioned saving efforts can fall short.

❌ Mistake 1: Waiting Too Long to Start Saving

One of the biggest mistakes parents make is delaying college savings until their children are older.

When children are young, college may feel far away, and families often focus on more immediate expenses such as childcare, housing, or daily living costs. Unfortunately, delaying savings reduces the time available for investments to grow.

Illustration: Starting Early vs Starting Late

| Age Child Starts Saving | Monthly Savings | Estimated Balance at 18 |

|---|---|---|

| Age 1 | $200 | ~$77,000 |

| Age 10 | $200 | ~$24,000 |

This simplified example demonstrates how compound growth works. Starting early allows small monthly contributions to grow significantly over time.

Parents who wait until high school may find themselves rushing to save large amounts in a short period.

❌ Mistake 2: Underestimating the True Cost of College

Another common mistake is assuming tuition is the only expense involved.

In reality, the full cost of college includes:

-

Tuition and fees

-

Housing and meals

-

Books and supplies

-

Transportation

-

Personal expenses

When all these costs are combined, the total price of a four-year degree can easily reach six figures.

Typical Breakdown of College Costs

| Expense Category | Approximate Share |

|---|---|

| Tuition & fees | 40% |

| Housing & meals | 30% |

| Books & supplies | 10% |

| Transportation | 10% |

| Personal expenses | 10% |

Shown above are rough figures and this may chnage based on the state university and other factors.

Many families focus only on tuition when estimating college costs. This can create a financial gap when additional expenses appear later.

❌ Mistake 3: Not Using Tax-Advantaged Education Accounts

Many parents save for college in regular savings accounts, missing out on potential tax advantages.

Education-focused accounts can offer benefits such as tax-free growth or tax-deductible contributions depending on the program. These accounts are specifically designed to help families save for education expenses.

Across the United States, more than 16 million education savings accounts exist, holding over $500 billion in assets, with an average balance of about $30,295.

Despite these advantages, awareness remains low. Surveys show that more than half of parents are unfamiliar with education savings programs designed for college planning.

Without using tax-efficient savings strategies, parents may lose potential growth that could help offset rising tuition costs.

❌ Mistake 4: Sacrificing Retirement Savings for College

Parents often feel responsible for covering most of their child’s college expenses. In fact, 95% of parents expect to pay for more than half of their child’s college costs.

However, prioritizing college savings over retirement can create long-term financial risks.

Unlike college, retirement has no scholarships or student loans. Financial experts generally recommend ensuring retirement savings are on track before committing large amounts to college funds.

Parents who sacrifice retirement contributions may struggle financially later in life, potentially becoming dependent on their children.

❌ Mistake 5: Ignoring Financial Aid Opportunities

Many parents assume they will not qualify for financial aid and therefore do not explore scholarships, grants, or assistance programs.

In reality, financial aid plays a significant role in helping families pay for college. Research shows that:

-

60% of families receive scholarships

-

57% receive grants

Both of these forms of aid reduce the amount families must pay out of pocket.

Parents who overlook these opportunities may miss valuable funding sources that could significantly reduce education costs.

Sources of College Funding

| Source | Percentage Contribution |

|---|---|

| Family income & savings | Largest share |

| Scholarships & grants | Major support |

| Student borrowing | Moderate |

| Other support | Smaller share |

Planning for financial aid early can reduce financial pressure later.

❌ Mistake 6: Not Talking to Children About College Costs

College planning should involve the entire family, including students themselves.

Research shows that 67% of students and 70% of parents have discussed how they will finance college, but many families still lack clear expectations about financial responsibilities.

When families avoid these conversations, students may apply to schools that are financially unrealistic.

Open discussions about budgets, savings, and potential financial aid options can help students make more informed decisions about their education.

❌ Mistake 7: Relying Too Much on Student Loans

Student loans are often used to bridge the gap between savings and college costs. While borrowing can be helpful, relying too heavily on loans can create long-term financial challenges.

Many students graduate with significant debt that may take years to repay. Some families underestimate how quickly student loan balances can grow.

A balanced approach that combines savings, financial aid, and responsible borrowing can help reduce long-term debt.

A Balanced College Funding Strategy

| Funding Source | Example Share |

|---|---|

| Parent savings | 40% |

| Scholarships & grants | 30% |

| Student contribution | 10% |

| Loans | 20% |

This diversified strategy helps families avoid excessive borrowing while still supporting educational goals.

❌ Mistake 8: Not Adjusting the Plan Over Time

College savings plans should not remain static.

As children grow older, family income, investment performance, and education goals may change. Regularly reviewing savings progress allows parents to adjust contributions, investment strategies, and financial expectations.

Families that revisit their plan annually are more likely to stay on track and avoid surprises when college enrollment approaches.

Practical Steps to Avoid These College Savings Mistakes

Parents can improve their college savings strategy by following a few simple principles.

✅ Start saving early – Even small monthly contributions can grow significantly over time.

✅ Use tax-efficient education accounts – Specialized education savings accounts may provide tax advantages and investment growth.

✅ Review financial plans regularly – Updating savings strategies helps families stay aligned with changing goals and costs.

✅ Explore scholarships and financial aid- These resources can reduce out-of-pocket expenses significantly.

✅ Maintain a balance between college savings and retirement planning – Protecting long-term financial security should remain a priority.

Checklist for Smart College Saving

Use this simple checklist to stay on track when planning for your child’s college education.

☑ Step 1: Estimate future college costs

Research current tuition rates and project how costs may increase over the next 10–18 years.

☑ Step 2: Start saving as early as possible

The earlier you begin saving, the more time your money has to grow through compound interest.

☑ Step 3: Use education savings accounts

Consider tax-advantaged options like a 529 college savings plan or other education-focused savings tools.

☑ Step 4: Review progress each year

Check your savings progress annually and adjust contributions based on changes in income, expenses, or tuition trends.

☑ Step 5: Research scholarships and financial aid

Look for grants, scholarships, and financial aid opportunities early to reduce the total amount you need to save.

Key Takeaways for Parents Planning College Savings

Saving for college is an important financial goal, but it requires thoughtful planning and realistic expectations. Parents who start early, use tax-efficient savings tools, and explore financial aid opportunities are more likely to reduce financial stress when their children reach college age. Avoiding common mistakes can make a significant difference in how prepared families feel when the time comes to pay for higher education.Ultimately, the goal is not only to fund a college education but also to maintain long-term financial stability for the entire family. With the right planning and consistent saving habits, families can build a stronger financial foundation for their children’s future.

Sources:

- Education Data Initiative – College Savings Statistics

- Sallie Mae – How America Pays for College 2025

- Fidelity College Savings Study

- Forbes – College Savings Trends

- Investopedia – How Families Pay for College

- T. Rowe Price – College Cost Benchmarks