Key Points

- Sinking Funds vs. Emergency Funds: Unlike an emergency fund for “just in case” crises, a travel sinking fund is a targeted, “when and where” savings bucket specifically designed to pre-pay your 2027 vacation without touching your safety net.

- The “Runway” Advantage: Starting today gives you a 24 to 30-month runway, allowing you to fund a $5,000 trip with manageable monthly contributions as low as $166, rather than facing a high-interest credit card bill later.

- Strategic Growth with HYSAs: By moving your travel fund into a High-Yield Savings Account (HYSA), you can leverage 2026’s competitive 4.5% interest rates, essentially letting the bank pay for your excursions and extra meals.

Planning a vacation is usually the highlight of the year, but for many Americans, the “vacation hangover” of credit card debt is a reality that lingers long after the tan fades. Recent economic data suggests that travel costs have shifted significantly. According to the U.S. Bureau of Labor Statistics, while overall inflation has shown signs of stabilizing at 3.1%, the cost of “transportation services”—which includes airfare—remains a volatile variable for household budgets. Furthermore, recent consumer surveys indicate that nearly 36% of travelers planned to go into debt to fund their summer trips, with the average vacation costing upwards of $1,900 per person. If you are looking toward a milestone trip in 2027, the secret to a stress-free departure isn’t a higher credit limit; it is the strategic implementation of a travel sinking fund.

The Psychology of the Sinking Fund Versus Traditional Savings

A sinking fund is fundamentally different from an emergency fund. While an emergency fund is a “just in case” safety net for the pipe that bursts or the sudden job loss, a sinking fund is a “when and where” tool. It is a targeted savings category for a specific, looming expense. By labeling your savings specifically for a 2027 vacation, you switch your brain from a state of deprivation to a state of anticipation. Behavioral economics shows that we are much more likely to stay consistent with a goal when it is visualized. When you move money into a travel sinking fund, you aren’t “losing” that money for current spending; you are pre-purchasing your future relaxation. This psychological shift reduces the friction of saving because the reward is clearly defined.

Related: Planning a Major Life Event? Try a Sinking Fund

Related: Planning a Major Life Event? Try a Sinking Fund

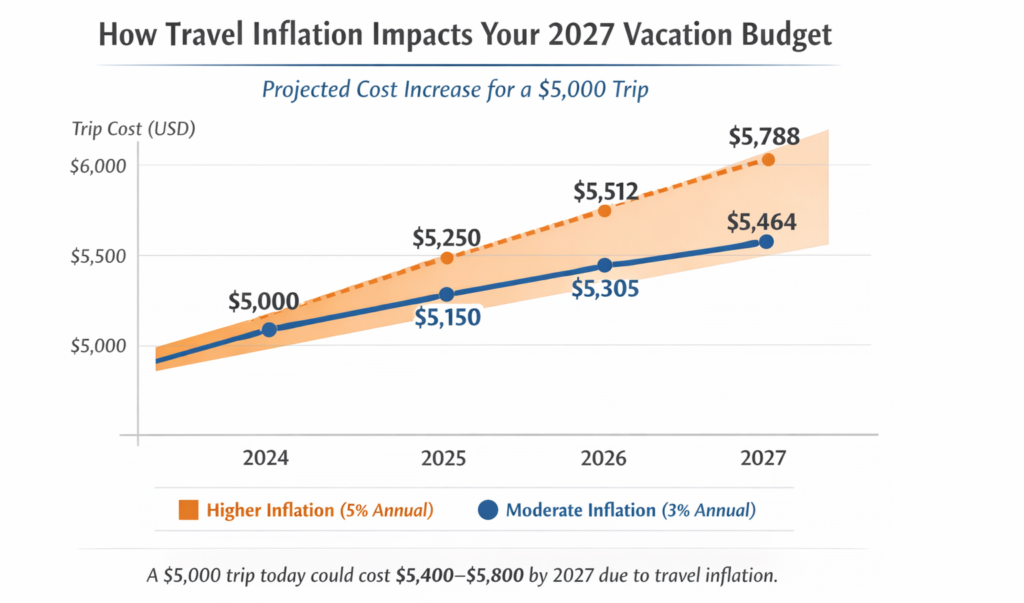

Understanding the Impact of Travel Inflation on 2027 Goals

When we plan for a trip two or three years away, we often make the mistake of using today’s prices as our final benchmark. However, the travel industry is particularly sensitive to fluctuations in fuel costs, labor shortages, and seasonal demand. Historically, travel costs tend to rise at a rate that slightly outpaces general inflation.

If you were to book a mid-range European excursion today for $5,000, that same itinerary in 2027 might require an additional $400 to $600 to maintain the same level of quality. By factoring in a 3% to 5% annual inflation buffer now, you ensure that you won’t have to downgrade your hotel or skip a bucket-list tour because of a price hike that happened while you were saving. This data-driven foresight is what separates a strategic saver from a reactionary spender.

Mapping Your 2027 Destination Costs

To save effectively, you need a target that reflects the reality of 2027 prices. If a trip costs $4,000 today, you must account for a modest inflation buffer. When mapping your costs, break them down into five non-negotiable categories: transportation, lodging, food and drink, activities, and the “miscellaneous” buffer. The buffer is crucial because it covers the hidden costs like passport renewals, travel insurance, and international phone plans that often get ignored in the initial excitement of planning.

Creating Your Monthly Contribution Blueprint

The beauty of a 2027 goal is the luxury of time. The longer your “runway,” the smaller your monthly “takeoff” amount needs to be. If you start today, you likely have around 24 to 30 months to prepare. Breaking a large $5,000 goal into monthly increments makes it feel like a manageable utility bill rather than an insurmountable mountain. Below is a roadmap of how monthly contributions change based on your total goal and the time you have remaining:

| Total Goal | 12 Months Out | 24 Months Out | 30 Months Out |

| $2,500 | $208.33 | $104.17 | $83.33 |

| $5,000 | $416.67 | $208.33 | $166.67 |

| $7,500 | $625.00 | $312.50 | $250.00 |

| $10,000 | $833.33 | $416.67 | $333.33 |

Selecting the Right Financial Vehicle

Where you park your sinking fund is just as important as how much you put in it. Keeping your travel fund in your primary checking account is a recipe for accidental spending. Instead, utilize a High-Yield Savings Account (HYSA) that is completely separate from your daily bank. As of early 2026, many HYSAs are still offering competitive rates above 4%. If you save $5,000 over two years in an account earning 4.5% interest, you could earn over $230 in interest alone. That is essentially a “free” dinner or an extra excursion paid for by the bank. Ensure the account has no monthly fees and allows you to create “buckets” or “vaults” so you can see your “2027 Dream Trip” label every time you log in.

The Hidden Vacation Costs Most Sinking Funds Forget

A common pitfall in vacation planning is focusing solely on the big-ticket items like flights and hotels while neglecting the “administrative” costs of travel. For a 2027 international trip, have you checked your passport expiration date? Renewals currently cost $130, and if you wait until the last minute, expedited fees can double that.

Furthermore, travel insurance is no longer a luxury but a necessity in a post-pandemic world, often costing between 5% and 10% of your total trip cost. Other “invisible” drains include pet boarding fees, which can easily run $50 to $100 per night, and international roaming charges if your phone plan isn’t optimized. By building these into your sinking fund now, you avoid the “last-minute scramble” that usually results in high-interest credit card swipes.

The Data Driven Audit for Travel Cash

To fund this account without feeling the squeeze, you need to perform a cash leak audit. We often ignore small, recurring costs that, when redirected, could fund an entire flight. For example, a $15 monthly streaming service you rarely watch equals $360 over 24 months.

If you find four such “leaks,” you have already funded nearly $1,500 of your 2027 trip. Look specifically at “loyalty penalties” in your internet and insurance bills. Spending one afternoon calling providers to negotiate rates can often yield $50 to $100 in monthly savings. Redirect that found money immediately via an automated transfer to your sinking fund so you never even see it in your checking account.

Case Study: Three Paths to the $5,000 Milestone

To visualize how this works in the real world, consider three different household profiles aiming for a $5,000 vacation in 24 months.

The “Aggressive Auditor” finds $210 a month by cutting three major streaming services, switching to a generic grocery list, and canceling a little-used gym membership. They hit their goal precisely on time without changing their primary income.

The “Windfall Warrior” contributes only $100 a month from their paycheck but commits to moving 100% of their annual tax refund and work bonuses into the fund.

Finally, the “Side Hustle Strategist” dedicates 10 hours a month to a freelance gig, depositing the entire $250 net profit into their HYSA, hitting the goal four months early. Each path is valid; the only requirement is consistency.

Automating Your Consistency

Human willpower is a finite resource, but automation is infinite. The most successful savers are those who treat their sinking fund like a mandatory tax. Set up a recurring transfer to trigger on the day your paycheck hits your account. By automating the process, you remove the “decision fatigue” of saving. You won’t have to ask yourself if you can afford to save this month; the money is gone before you can spend it on something impulsive. This “pay yourself first” mentality is the cornerstone of strategic travel planning.

The Power of Compound Interest on Long-Term Goals

While two years might feel like a short time, it is enough time for compound interest to start showing its teeth. When you use a High-Yield Savings Account, the bank pays you interest on your principal, and then in the following month, they pay you interest on your principal plus the interest you earned the previous month. On a $5,000 goal, the difference between a standard 0.01% savings account and a 4.5% HYSA is hundreds of dollars. This is essentially the travel industry’s version of a “buy one, get one free” deal on a luxury meal or an upgraded room. By choosing the right financial vehicle today, you are essentially letting the bank contribute to your vacation fund on your behalf.

Strategic Hacks to Accelerate the Fund

- Use windfall money like tax refunds, work bonuses, or unexpected cash gifts to boost your travel fund

- Redirect cash-back rewards from credit cards into your sinking fund (only if you pay your balance in full each month)

- Set a habit of transferring accumulated rewards quarterly to build momentum

- Try a “no-spend month” once or twice a year to cut all non-essential expenses

- Channel the money saved during no-spend periods directly into your vacation fund

- Combine small savings strategies to create powerful bursts of progress

- Use these occasional boosts to reduce your overall saving timeline by several months

Monitoring and Adjusting for 2027 Realities

A sinking fund is not a “set it and forget it” tool; it requires a quarterly check-in. As 2027 approaches, travel trends may shift. If hotel prices in your chosen destination spike, you may need to adjust your monthly contribution by $20 or $30. Conversely, if you manage to find a great deal early, you can reduce your contributions and breathe easier. Being data-driven means being flexible. Use a simple spreadsheet to track your progress against your goal so you stay motivated by the visual evidence of your growing fund.

The Emotional Dividend of Debt Free Travel

✔ Travel without the stress of coming home to a credit card bill

✔ Avoid paying for your vacation months—or even years—after it ends

✔ Eliminate high-interest charges that can turn small expenses into big financial burdens

✔ Fully enjoy your memories without financial anxiety lingering in the background

✔ Experience a true “vacation high” that doesn’t fade due to money worries

✔ Give your future self peace of mind and financial freedom

✔ Make every no-spend weekend and budgeting effort feel worthwhile

✔ Return home feeling relaxed—not financially pressured

Final Thoughts on Stress Free Travel

The ultimate goal of a travel sinking fund is to ensure that when you are sitting on that beach or exploring that ancient city in 2027, you are truly present. You aren’t worrying about the bill coming in the mail or how you will pay for the meals you are eating. You have already done the hard work. You have audited your leaks, automated your growth, and strategically planned for inflation. By starting today, you aren’t just saving money; you are buying the peace of mind that makes a vacation truly feel like a getaway.

Sources:

-

U.S. Bureau of Labor Statistics: Consumer Price Index Summary (bls.gov)

-

Federal Reserve Board: Report on the Economic Well-Being of U.S. Households (federalreserve.gov)

-

Consumer Financial Protection Bureau: Tips for Targeted Savings (consumerfinance.gov)

-

U.S. Department of State: Passport Fees and Processing Times (travel.state.gov)