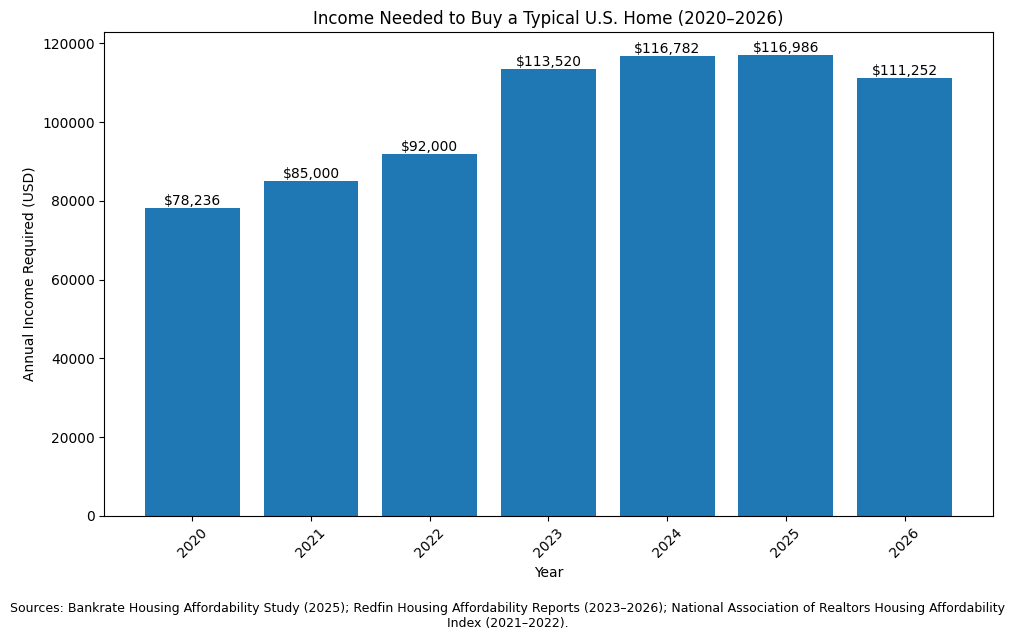

When I first started thinking about buying a house, the numbers sounded intimidating. According to a 2025 Bankrate study, Americans need an annual household income of roughly $117,000 to afford a typical U.S. home. The income needed to buy a home has risen much faster than median wages in recent years, but that doesn’t mean homeownership is out of reach with the right plan. In fact, affordability has recently improved somewhat — as of early 2026, buyers need an estimated $111,252 per year to afford the typical home, down about 4 % from the previous year’s peak. That still feels high compared with many households’ incomes, but the trend suggests there are ways to work toward ownership even without a “huge” salary.

In this article, I’ll share surprising ways I—and many others—approached home buying without needing an astronomical income, including actionable strategies to build savings, find affordable options, and make your path to ownership realistic.

Why the Numbers Sound Scary (But Don’t Tell the Whole Story)

It’s true that national averages suggest you need a six-figure income to afford many homes — but average doesn’t mean universal. Housing markets vary widely across the U.S., and many buyers leverage strategies like adjusting location priorities, increasing down payment flexibility, and seeking government programs to bridge gaps between income and purchase power.

Here’s a snapshot of what “typical” incomes and affordability look like:

| Measure | What It Represents | Approximate Figure |

|---|---|---|

| Annual income needed to afford median U.S. home (2025) | Nationwide estimate | ~$116,986 |

| Recent 2026 improvement estimate | Nationwide estimate | ~$111,252 |

| Median U.S. household income (2023) | Typical earnings | ~$80,000-$86,000 (varies by source) |

| Percentage of homes priced out of reach | Households unable to afford median home | ~75 % |

Seeing this comparison helped me realize that income alone doesn’t determine my ability to buy. What strategy I used made the difference.

Start With a Flexible Definition of “Home”

When most people imagine buying a house, they picture a detached single-family home in a specific neighborhood. That dream might still be attainable in time, but narrowing your search to a specific price range or type of property first can make ownership much more realistic.

Here are common types of homes to consider:

| Housing Option | Typical Cost Range | Why It’s Worth Exploring |

|---|---|---|

| Starter single-family homes | $250,000-$350,000 | Lower cost and good long-term investment |

| Townhouses/row homes | $200,000-$300,000 | Often more affordable than detached homes |

| Condos/co-ops | $150,000-$280,000 | Lower maintenance and HOA fees |

| Fixer-uppers | Varies | Lower purchase price but higher upfront work |

| Manufactured/modular homes | $100,000-$250,000 | Lower entry costs |

This table helped me think beyond a narrow price bucket and explore alternatives that fit my budget now.

Build Savings With Smart Budget Moves

A down payment and other upfront costs (closing fees, inspections, insurance) are often the biggest obstacle for first‐time buyers. Even a modest down payment can make homeownership possible.

Here’s how I organized my savings goals:

| Savings Category | Target | Strategy Used |

|---|---|---|

| Down payment | 10 %-15 % of home price | Automatic monthly transfer to savings |

| Closing costs | 2 %-5 % of home price | Budget line item tracked separately |

| Emergency fund | 3-6 months expenses | Reduced risk of dipping into home savings |

| Homeownership expenses | Established reserve | Saved for utilities, repairs |

One of the most effective moves was setting up automated savings transfers. I treated my future home purchase like a bill I already owed to myself.

Leverage First-Time Buyer Programs

Many homeowners use assistance programs to bridge income gaps or reduce upfront costs. These can include:

| Program Type | What It Helps With | Example |

|---|---|---|

| Down payment assistance | Grants or low-interest loans | Various state/local programs |

| FHA loans | Lower down payments (as low as 3.5 %) | Federally insured mortgages |

| VA loans | No down payment for eligible veterans | U.S. Department of Veterans Affairs |

| USDA loans | Low-income rural housing help | U.S. Department of Agriculture |

Sources: Home Buying Government Assistance Programs

FHA Loans – U.S. Department of Housing and Urban Development

VA Home Loans -Veterans Benefits Administration

Single Family Housing Guaranteed Loan Program

Consider Timing and Market Trends

Mortgage rates and market conditions change over time. When I was shopping, I monitored trends before making a move. In some periods, slight declines in required income — like the recent drop from over $115,000 to around $111,000 — made offers more viable for buyers on the edge of qualifying.

📈 Income Needed to Afford a Typical U.S. Home — 2020 to 2026 (National Estimates)

Adjust Your Priorities (and Budget)

A big part of my success came from making clear choices about what mattered most:

-

I chose a neighborhood with slightly lower demand to get more square footage for the price.

-

I reduced discretionary spending and redirected it to my savings goal.

-

I compared loan options and worked with lenders to optimize my down payment and interest rate scenarios.

-

I built in a cushion for property taxes and insurance so I wasn’t stretched thin after buying.

This comparison helped me see that where and how I bought mattered as much as whether I could afford it:

| Priority | Higher Cost Choice | Lower Cost But Still Good |

|---|---|---|

| Home size | Larger home | Smaller home or condo |

| Location | High-cost metro | Suburban or emerging metro |

| Down payment | 20 % | 10 % with assistance |

| Mortgage | Fixed high rate | Explore adjustable/discounted options |

These strategic choices made what felt impossible achievable.

Homeownership Is a Journey, Not an Instant Decision

One of the most important realizations was accepting that buying a home may take time. It wasn’t about having the perfect income right this second — it was about preparing financially and making smart decisions along the way.

For some buyers, that meant:

-

Renting longer to save more upfront

-

Targeting homes with future value growth

-

Teaming up with a financial advisor or housing counselor

-

Taking advantage of state/local programs and timing incentives

Think beyond the headline numbers

Affording a home today may require higher income than in the past — but it doesn’t require an astronomically huge salary. With deliberate planning, flexibility, and smart use of available resources, homeownership can be within reach for many households. Affordability may still vary widely across cities and states — and not every market will be friendly — but understanding what’s needed and how to work toward it is the first step.

Think beyond the headline numbers. Your strategy could be just as important as your paycheck when it comes to buying a home.