Disclaimer:

The information provided on MyAmericanSavings.us is for educational purposes only and should not be construed as financial, investment, or legal advice. Please consult with a licensed professional before making any financial decisions.

Key points:

➜ Not every unexpected expense is a true emergency. Always evaluate if the cost is urgent, necessary, and unavoidable before using your emergency fund.

➜Explore other financial options first. Budget adjustments, payment plans, or insurance coverage may help you handle expenses without draining your savings.

➜ Protect and rebuild your safety net. If you must use your emergency fund, create a plan to replenish it so you remain financially prepared for future emergencies.

Unexpected expenses can hit anyone. A medical bill, car repair, or sudden job loss can quickly disrupt even the best financial plans. That’s exactly why emergency funds exist — to provide a financial cushion when life becomes unpredictable. The below representation graphic shows a simple visual of emergency savings situations among Americans. Each row represents a financial situation, and the blue circles act like bars in a bar chart.

Have enough savings for 3 months – 46%

Used emergency savings last year – 37%

Cannot cover a $400 emergency – 29%

Have no emergency savings – 24%

A recent survey found that only 46% of Americans have enough savings to cover a $1,000 emergency expense, while nearly 24% have no emergency savings at all. In addition, 37% of people needed to tap their emergency savings in the past year for unexpected costs such as bills, repairs, or daily expenses.

Another report shows that one in three Americans has no emergency savings, and nearly 29% say they cannot afford an unexpected expense over $400.

These numbers highlight an important truth. Building an emergency fund is only half the battle. The real challenge is knowing when to use it.

This is where the emergency fund test comes in. Before touching your savings, asking a few key questions can help protect your financial safety net and prevent unnecessary withdrawals.

Related: From $0 to $1,000: How I Built My Emergency Fund

Related: From $0 to $1,000: How I Built My Emergency Fund

How to Save Money for Emergency Funds?

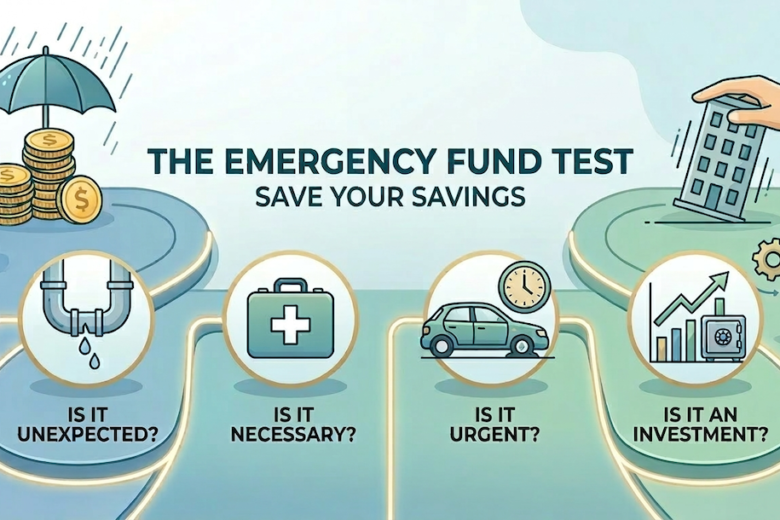

Question 1: Is This Truly an Emergency?

Not every unexpected expense qualifies as a real emergency. A genuine financial emergency typically meets three conditions:

✓ It is unexpected

✓ It is urgent

✓ It is necessary

Examples of real emergencies include sudden medical bills, essential home repairs, or job loss.

Expenses such as holiday shopping, vacations, or upgrading gadgets usually do not qualify. Using emergency savings for non-essential purchases can weaken your financial safety net and leave you vulnerable when a real crisis occurs.

Quick Emergency Test Checklist

| Question | If Yes | If No |

|---|---|---|

| Is the expense unexpected? | ✅ Continue evaluating | ❌ Not an emergency |

| Is it urgent? | ✅ Continue evaluating | ❌ Consider saving instead |

| Is it necessary for survival or safety? | ✅ Likely an emergency | ❌ Avoid using emergency fund |

Question 2: Can This Expense Be Covered by Your Regular Budget?

Sometimes what feels like an emergency is actually a budgeting issue.

For example, annual expenses such as insurance premiums, school supplies, or car maintenance are predictable costs. Instead of using emergency savings, these expenses should ideally be planned in advance within a monthly or sinking fund budget.

Many households mistakenly treat predictable costs as emergencies, which gradually drains their savings over time.

Budget vs Emergency Expense Comparison

| Expense Type | Emergency Fund? | Budget Category? |

|---|---|---|

| Job loss | Yes | No |

| Emergency surgery | Yes | No |

| Routine car maintenance | No | Yes |

| Holiday travel | No | Yes |

| Home appliance breakdown | Often yes | Sometimes |

If the expense could have been predicted months earlier, it is usually better handled through budgeting rather than emergency savings.

Question 3: Do You Have Other Financial Options?

Before touching your emergency fund, it is worth exploring other solutions.

Some possible alternatives include:

• Adjusting discretionary spending temporarily

• Using a short-term sinking fund

• Negotiating payment plans for medical bills

• Using insurance coverage

This does not mean taking on risky debt, but sometimes a temporary financial adjustment can protect your long-term savings.

For instance, negotiating a payment plan with a hospital may allow you to spread costs over several months without draining your emergency fund in a single payment.

Alternative Solutions Chart

| Alternative Option | When It Works |

|---|---|

| Payment plan | Medical bills or large invoices |

| Insurance coverage | Accidents, health costs, property damage |

| Temporary budget cuts | Short-term expenses |

| Side income | Non-urgent expenses |

If a safer financial solution exists, it may be better to preserve your emergency savings.

Question 4: Will This Expense Affect Your Financial Stability?

Another important question to ask is whether avoiding the expense could lead to bigger problems later.

For example:

Ignoring a roof leak may lead to major structural damage.

Skipping essential car repairs could make your vehicle unsafe to drive.

Avoiding medical treatment could worsen a health condition.

In these situations, using your emergency fund is not only reasonable but responsible.

Emergency funds are meant to prevent financial crises from becoming disasters.

Cost of Delaying Repairs (mentioned are rough figures and may vary)

| Issue | Immediate Cost | Cost if Ignored |

|---|---|---|

| Roof leak repair | $400 | $3,000 structural damage |

| Car brake repair | $250 | $1,500 accident repair |

| Minor plumbing leak | $150 | $2,000 water damage |

Sometimes spending from your emergency fund today prevents much larger expenses tomorrow.

Question 5: How Quickly Can You Rebuild the Fund?

Using emergency savings is sometimes unavoidable. But before making a withdrawal, it is wise to consider how quickly the fund can be rebuilt.

Financial experts typically recommend saving three to six months of essential living expenses as a safety buffer.

If using part of your savings leaves you with very little remaining protection, rebuilding the fund should become a priority.

Emergency Fund Recovery Plan:

✓ Calculate remaining emergency savings

✓ Set a monthly replenishment goal

✓ Automate savings transfers

✓ Reduce non-essential spending temporarily

✓ Direct bonuses or tax refunds into savings

A clear rebuilding plan ensures that a single emergency does not leave you financially exposed for months.

Question 6: Is This a One-Time Crisis or a Long-Term Issue?

Another important test involves identifying whether the problem is temporary or ongoing.

Emergency funds are designed for short-term financial shocks. However, if the expense reflects a long-term financial problem, simply withdrawing savings will not solve the underlying issue.

Examples include:

• Chronic overspending

• Structural income shortages

• Rising debt payments

• Lifestyle inflation

If the expense is part of a recurring financial pattern, it may require deeper changes such as budgeting adjustments or income growth strategies.

Emergency vs Structural Financial Problem

| Scenario | Emergency Fund? |

|---|---|

| Sudden medical expense | Yes |

| Temporary job loss | Yes |

| Overspending every month | No |

| Growing credit card debt | No |

Recognizing the difference can prevent repeated withdrawals that drain your savings completely.

Question 7: Would You Regret Using the Fund Later?

The final test is emotional but surprisingly powerful.

Imagine that a real crisis occurs next month. If your emergency fund were already depleted, would you regret using it for today’s expense?

If the answer is yes, it may be worth reconsidering the decision.

Emergency funds provide not only financial protection but also peace of mind. Many people underestimate the psychological security that comes from knowing they have a financial cushion available.

Studies show that households with emergency savings report significantly lower financial stress during economic downturns.

Protecting that sense of stability can be just as valuable as the money itself.

Your Emergency Fund Strategy Going Forward

Emergency funds are one of the most important pillars of financial security. They protect households from unexpected shocks, prevent debt accumulation, and provide peace of mind during uncertain times.

But using them wisely requires discipline and careful decision-making.

Before spending your emergency savings, pause and run through the emergency fund test. Asking the right questions can help you distinguish between true emergencies and temporary financial inconveniences.

The goal is not to avoid using your savings altogether. After all, emergencies happen. The real goal is to ensure that when you do use your emergency fund, it is for the right reasons.

When used thoughtfully, your emergency savings can do exactly what it was designed to do — protect your financial future.

Sources